Categories Economy

Let’s do an update and go through some exciting developments. In short, the picture for NatGas continues to improve from all angles.

A thread.

Time for a thread about US NatGas and why it will surprise to the upside...

— BVDDY (@BvddyCorleone) October 22, 2020

There\u2019s an exceptional opportunity setting up in the energy space, in particular for US NatGas and related equities.

I\u2019ll explain the setup in this thread and also reveal my top pick. \U0001f920

Easy as ABC. How to do it.

[THREAD]⚠️

#LockdownLevel3

#Bushiri

#RamaphosaChallenge

Go online to the website of CIPC and register a new company for R175, registration is R125 and the name is R50.

Go to https://t.co/RJcCHvdgCl which is the easiest website vision for CIPC.

These tax avoidance techniques result in effective tax rates of ~0-2.5% https://t.co/R433UuKInX

Multinationals played a crucial role in lifting Ireland out of the last recession and they will again as we rebuild our economy after Covid.\xa0What does SF want to do? Tax them.\xa0https://t.co/B7n8esbzPN

— Leo Varadkar (@LeoVaradkar) October 11, 2020

MNCs have been a bright spot in a faltering domestic economy during Covid lockdowns. They’ve provided a much-needed, reliable source of inflows as other streams have dried up.

However, we’re not 12 years old, so let’s have a deeper dive, as this is not showing the full picture.

Leo and his ilk will try to lightswitch-brain you into thinking that raising taxes on MNCs will drive them away. You should be grateful!

In reality, largest threat is from US and EU tax reform. Take Biden’s tax reform proposals, which targets US MNC offshoring/“GILTI” profits

GILTI, or Global Intangible Low-Taxed Income utilities “Base Erosion” or “BEPS” to lower the taxable profit in the United States by shifting ownership of US IP into Irish tax jurisdictions.

I would wager targeting these techniques is popular on both sides of the isle in America.

This represents a significant geo-political and economic risk for Ireland. At any moment, any change, whether intentional or accidental can change the incentive structures for US MNCs, resulting in these companies pulling billions of IP from Ireland over night.

V good points but overall I stick with the conclusion that this is a v risky deal.

— Alan Beattie (@alanbeattie) January 5, 2021

1. It\u2019s overstating it to say that COM now has final say over investment. FDI screening remains a MS competency. COM has had to take a v secondary supporting role over Huawei and 5G.

1/n https://t.co/RVg2jnoFgK

Also reading this from @gideonrachman on EU-China. My view (cynically?) - that EU-China is a deal that makes a lot of sense given a probably unresolvable trade policy superpower triangle with the US, and best for the EU to move while China will.

The US and EU roughly agree on China that it should do some things differently, but not really the details of what those are. Meanwhile the EU and US have long standing trade policy differences, which neither (or their key stakeholders) prioritise resolving.

For the EU, the China deal has sent a message to the new US administration, you can't just tell us what to do. And delivered some (probably marginal in reality) benefits to business. For China, this is the 3rd deal with EU or US in 12 months. Pretty clear strategy there.

The key assumption that lies at the heart of too much writing on EU-US relations is that the two should cooperate on trade. After 25 years of largely failing to do so, I'd suggest we might want to question that a bit more deeply.

I wanted to wrap up the year by writing about something I have been thinking about for the last few months:

Who owns the best businesses in the world?

I am trying to draw a line from inherited wealth of feudal lords to community-owned services with tokens.

The last 1,000 years can be roughly split into two 500-year chunks: feudalism & capitalism. Feudal lords controlled all of the land, farms, buildings and capital. This was passed down inside families and never distributed to the workers.

Capitalism totally changed that.

Risk, reward and ruin were separated when joint-stock companies became more common. The prerequisite for successful entrepreneurship shifted from inheritance to initiative.

People without wealth could access it and start new ventures.

Founders started founding new companies.

Equity compensation kicked off in the 1950s but it really went into overdrive when it was mixed with high-growth technology companies backed with high-risk equity bets. Silicon Valley perfected the art. Employees at many of the most successful technology companies became owners.

The SEC did two huge things this year. They raised the crowdfunding limit to $5m and introduced a proposal to allow gig workers to receive stock.

I predict that we will see competitors to Airbnb, Uber and DoorDash all take advantage of this

SEC: proposed pilot program to allow tech companies to pay gig workers up to 15% of their annual compensation in equity rather than cash https://t.co/EJjLWQatcr

— Jesse Walden (@jessewldn) November 24, 2020

https://t.co/hmAz0tsyuv

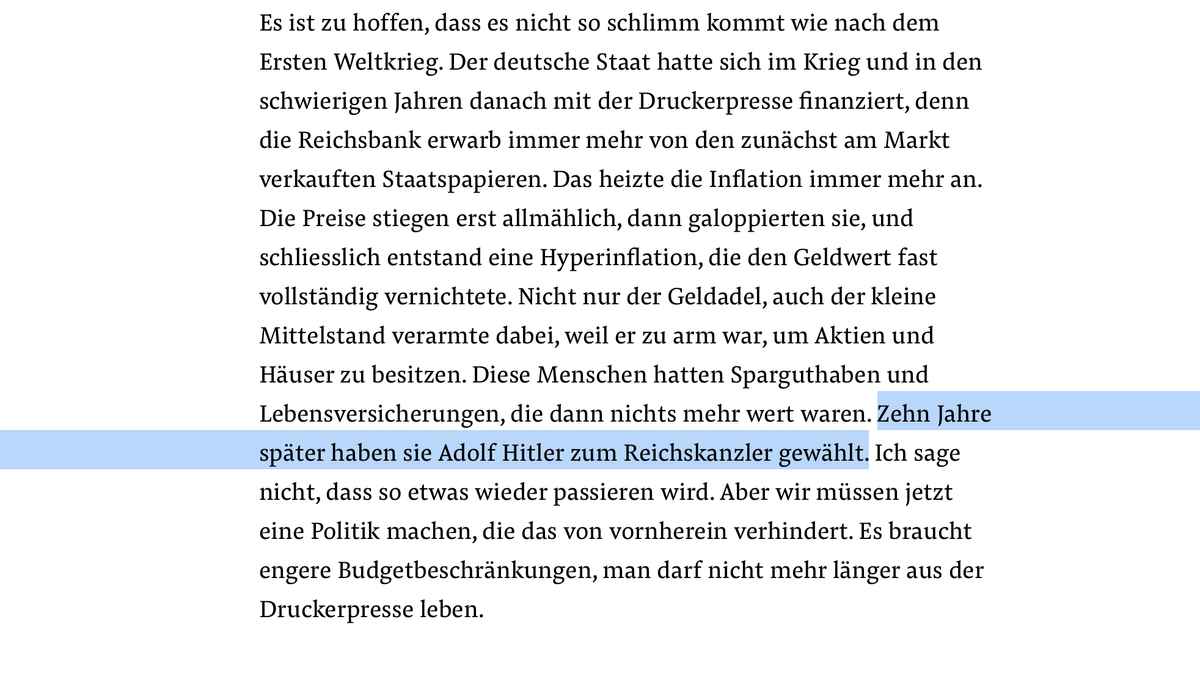

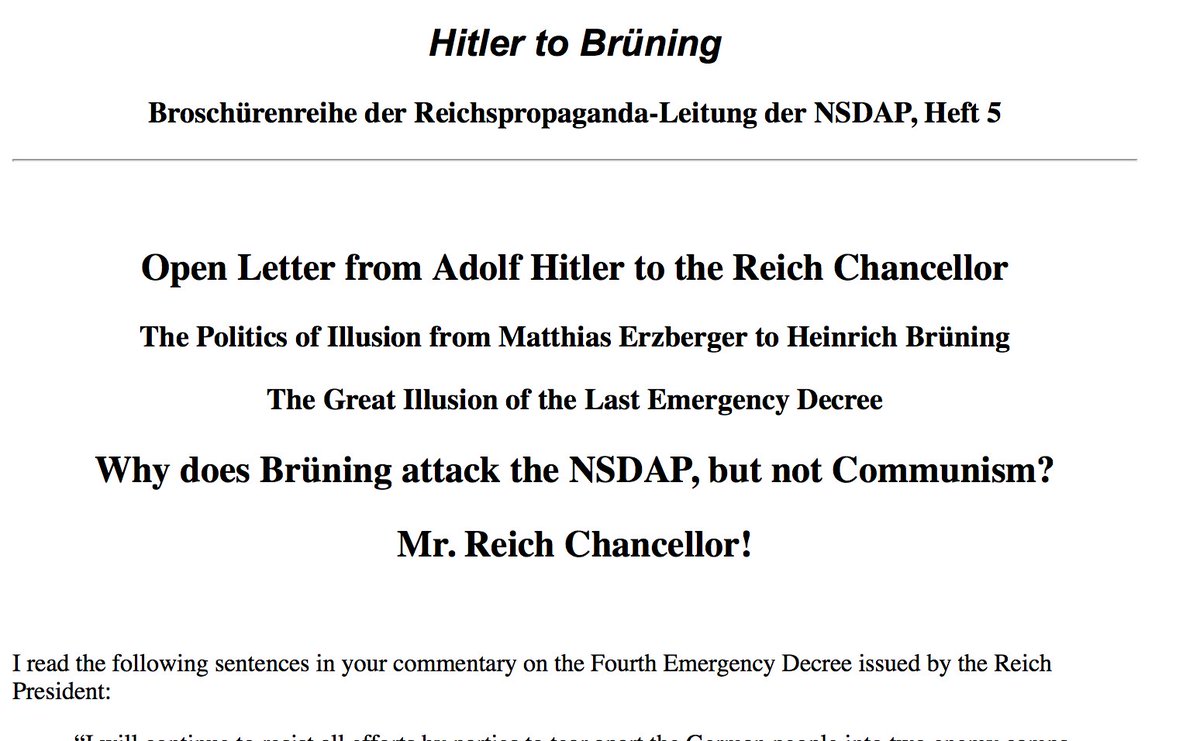

Sinn says hyperinflation after WW1 impoverished the German middle class in the Weimar Republic: "Ten years later they elected Adolf Hitler as Reich Chancellor." Policy recommendation today against hyperinflation: "tighter budget constraints" /2

https://t.co/ydfxgiCpkD

Sinn thus feeds a widespread misinterpretation. Mass poverty when the Nazis came to power in 1933 was not the result of hyperinflation, which at that time was ten years in the past; it was primarily a consequence of mass unemployment due to the recession in the early 1930s. /3

The Nazis had come to power after years of deflation - i.e. falling prices. From 1930 onwards, Reich Chancellor Brüning used emergency decrees to bring about tax increases and drastic state spending cuts that pierced the social safety net. /4

Austerity policies increased unemployment, led to social suffering and unrest. Hitler realised by the end of 1931 at the latest that Brüning's austerity policy would "help his party to victory and thus end the illusions of the present system." /5

https://t.co/yRN6hseciX

Obviously a longtime Disney D2C bull; I was astounded, shocked by slate's quality, range, volume.

This is Disney going beyond a digital "Vault" plus originals. It is saying all of your favorite stories, more,

This feels like the true unveiling of Disney+ versus April 2019, tbh

— Matthew Ball (@ballmatthew) December 10, 2020

2/ Not just a stronger Disney+, but one that hugely raises the tablestakes of competition, growth, press coverage, notability.

Paramount+ plans new Star Trek year round. Feels quaint now. Peacock will have a Jurassic Park + Fast series eventually.

In other words, the year-long Disney+ Open Beta attracted 87M subscribers.

— Chris Lacy (@chrismlacy) December 10, 2020

3/ In "Content, Cars, and Comparisons in the 'Streaming Wars'", I wrote about how Disney $1B in content spend gets several billion of equivalent spend through its resonance

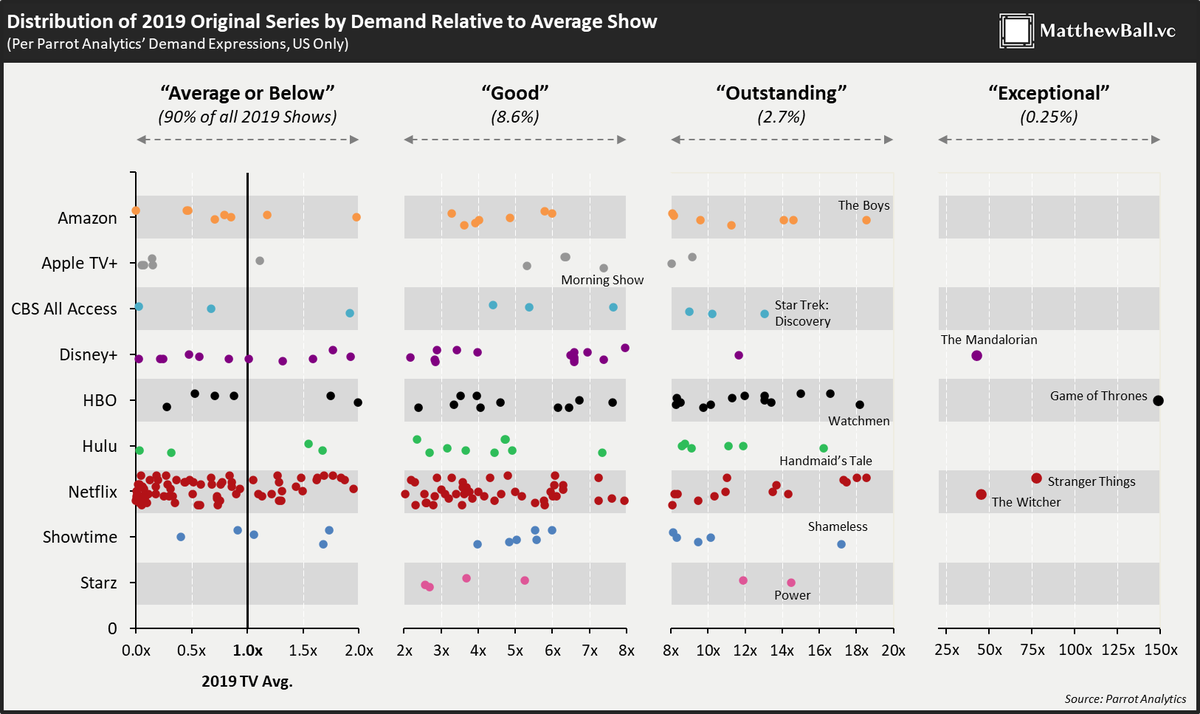

Mando was a top 5 show per @ParrotAnalytics in 2019. Disney thinks it can have 10 "Top 5s" a year.

4/ Trade talk can be misleading, but it takes only a cursory look at Twitter, the most popular shows of the past decade (Walking Dead, Thrones, Mando, Stranger Things), Disney's dominance at the box office (8 of top 10 in 2019) and wonder how to beat

A former exec at a global media giant: "This is how the game is now played. If other companies want to compete, this is now the threshold... it's a kind of cultural shock and awe" (With permission)

— Matthew Ball (@ballmatthew) December 11, 2020

5/ Roadmap doesn't just suck oxygen out of streaming wars (as Netflix did from 2014-18), it will enable Disney+ to rapidly grow its price

If I pay $54 a year to use Disney+ for 2 months, what happens when it's year-round?

Worth $15 month in

I pay $27 per month for Disney+. This is the biggest bull thesis for Disney.

— Matthew Ball (@ballmatthew) November 14, 2020