Long setup:

Trading a reversal using 3 bar Price Action

1. Bar 1 closes lower (Red)

2. Bar 2 closes below Bar 1 (Red)

3. Bar 3 closes above the high of both Bar 1 & Bar 2 (Green)

4. Buy at the close of bar 3

5. SL is low of Bar 3 & Trail SL

6. Decide position size as per risk

More from yashstocks

1/5

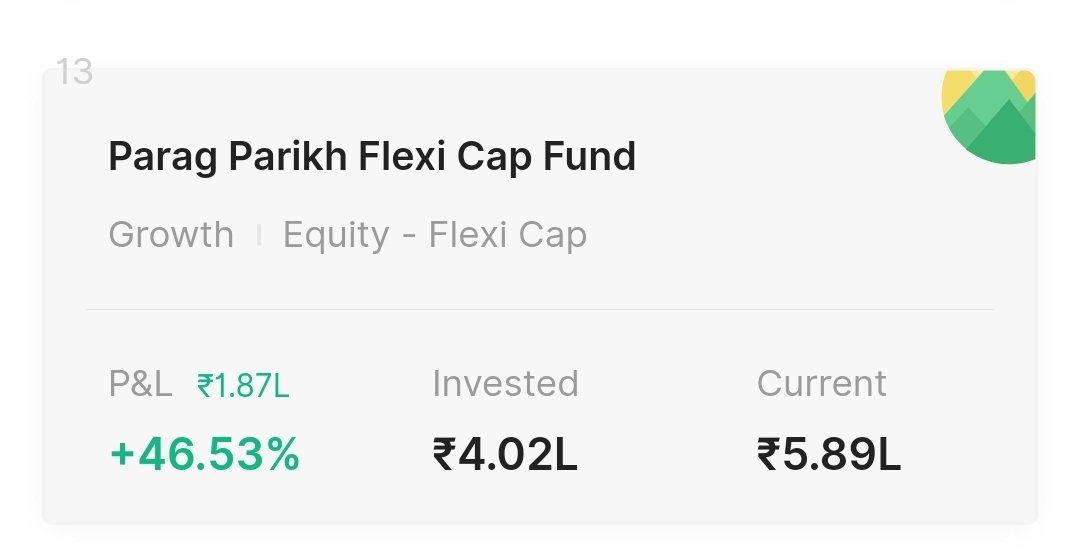

In equity funds, parag parikh flexi cap fund and mirae asset emerging bluechip funds are best. They have given superb returns in last 5 years.

Parag parikh flexi cap fund is diversified as it will invest in US stocks like Google, Facebook, Microsoft, Amazon along with Indian. https://t.co/RmoDMgXoRM

2/5

But one issue with this is if you exit before 2 years, there is an exit load of 2% in 1st year and 1% in 2nd year.

Mirae asset emerging bluechip funds stopped taking lump sum amounts and only can do SIP of Rs. 2500 currently.

3/5

But there is catch, you can do multiple SIPs in it, you can SIP on every day and still invest 75k in a month. I am doing this way only.

Coming to debt funds, ICICI prudential all seasons bond fund and hdfc corporate bond fund are good if consider 5 years performance.

4/5

In zerodha, all above 4 MFs can be pledged and haircut also very less just 7.5%. But you can use only 50% for positional margin, other 50% should come in cash or equivalent funds like gilt, liquid etc. For intraday, 100% can be used.

5/5

Nippon india gilt fund is also good, considering it will be cash component and only 10% haircut.

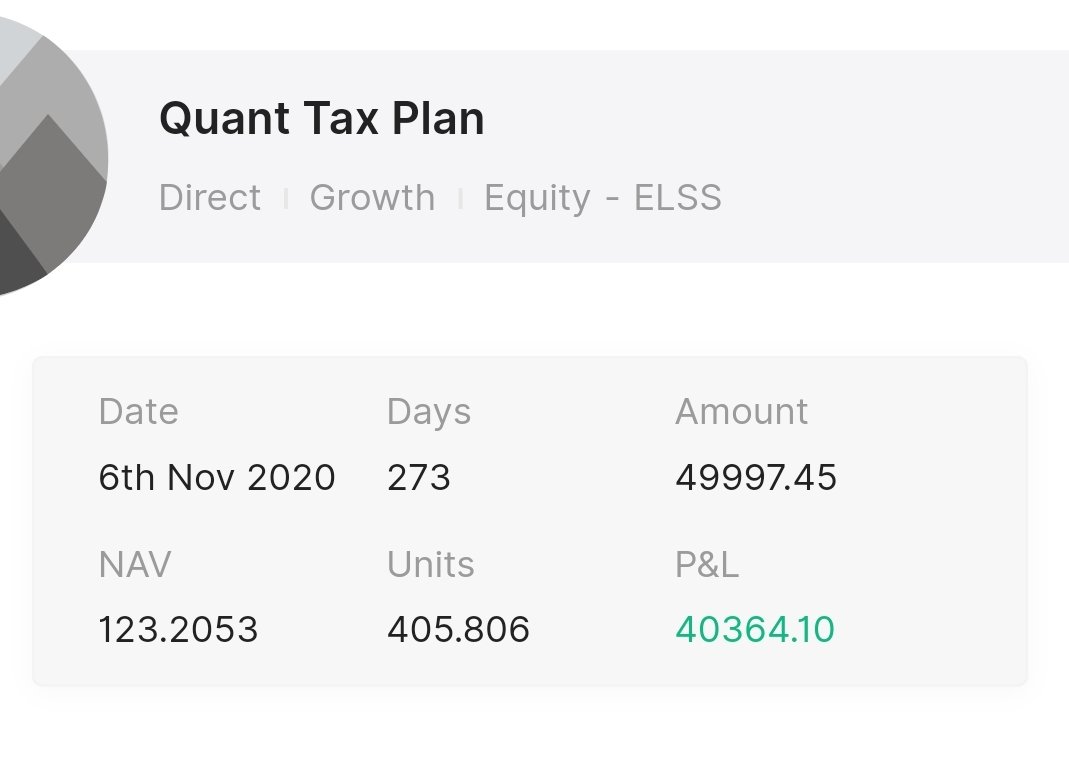

For tax saving, you need to invest in ELSS funds.

I invested in Quant Tax Plan and it gave 80% returns in just 273 days.

In equity funds, parag parikh flexi cap fund and mirae asset emerging bluechip funds are best. They have given superb returns in last 5 years.

Parag parikh flexi cap fund is diversified as it will invest in US stocks like Google, Facebook, Microsoft, Amazon along with Indian. https://t.co/RmoDMgXoRM

If I'm a layman in mutual fund territory N I wana invest Lumpsum of 1-2L N followed by SIP of 20k per month

— PythonTrader (Not a Python Coder) (@pythontrader999) August 6, 2021

1)Wat r the things I should look while scrutinising a MF

2)If I wana pledge it to broker so which kind of MF I should select @yashstocks@vishalmehta29@yogeshnanda1

2/5

But one issue with this is if you exit before 2 years, there is an exit load of 2% in 1st year and 1% in 2nd year.

Mirae asset emerging bluechip funds stopped taking lump sum amounts and only can do SIP of Rs. 2500 currently.

3/5

But there is catch, you can do multiple SIPs in it, you can SIP on every day and still invest 75k in a month. I am doing this way only.

Coming to debt funds, ICICI prudential all seasons bond fund and hdfc corporate bond fund are good if consider 5 years performance.

4/5

In zerodha, all above 4 MFs can be pledged and haircut also very less just 7.5%. But you can use only 50% for positional margin, other 50% should come in cash or equivalent funds like gilt, liquid etc. For intraday, 100% can be used.

5/5

Nippon india gilt fund is also good, considering it will be cash component and only 10% haircut.

For tax saving, you need to invest in ELSS funds.

I invested in Quant Tax Plan and it gave 80% returns in just 273 days.

More from Stockslearnings

🌟Lesson 1 - weekly /monthly breakout push stock price 30/50% higher in 2/3 weeks.

Ex- #sastasundar after breakout 145/155 zone , stocks in 2/3 weeks given 30/40% return.

And in 2/3 months it was double 💞 https://t.co/9kkc3IV4Lo

🌟Lesson 2 - if stock is making same pattern ( in 2 /3hours chart) after given breakout of (weekly /monthly chart) , then chances of stock going up is much more.

Ex - #HGS after given breakout of Trendline ( range) in monthly chart, again making same pattern 4 hours chart. 💞

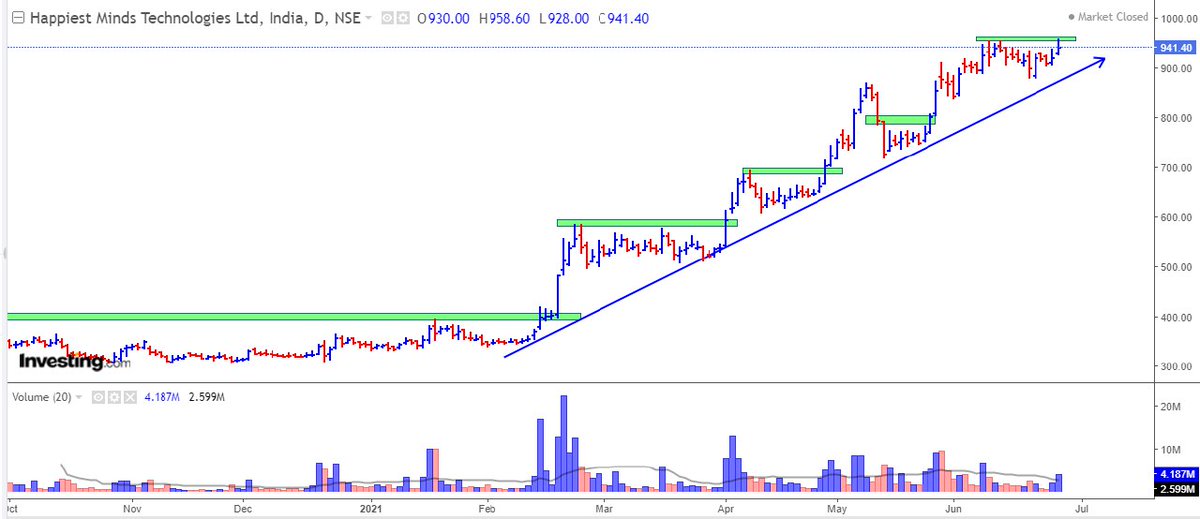

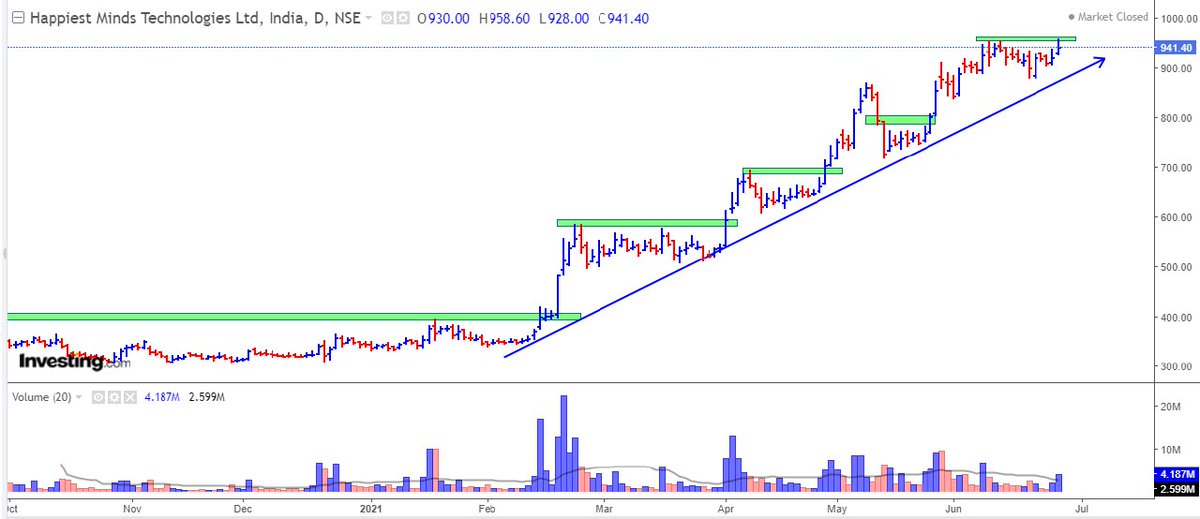

🌟Lesson 3- if stock never come to retest it's weekly & monthly breakout zone then the chances of it's 2x is much more.

EX - #happiestmind everytime consolidating & making new high. 💞

@chartmojo

@charts_breakout

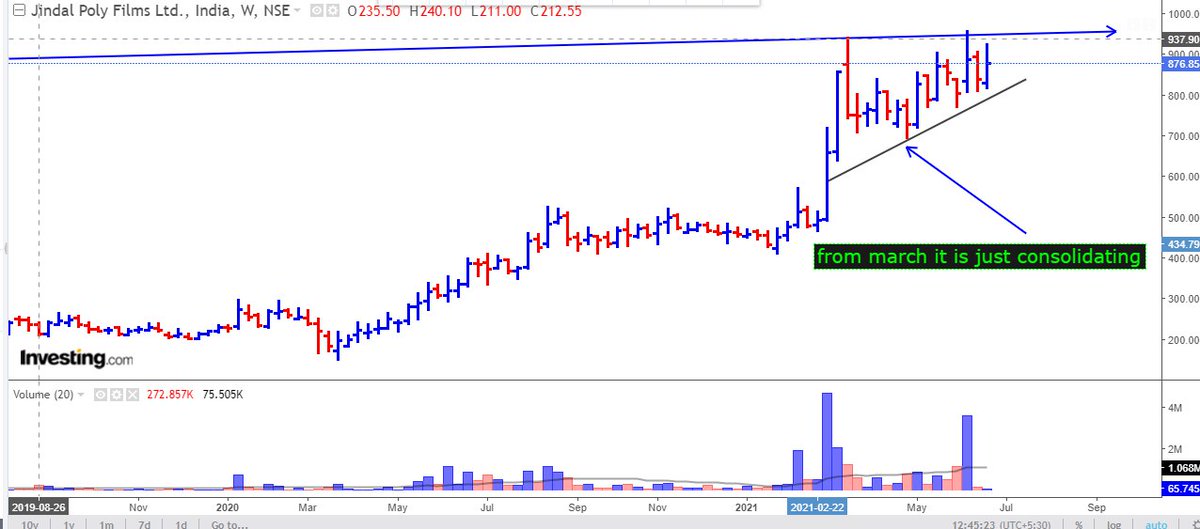

🌟Lesson 4 - when whole market fall still strongest stocks only consolidate or move down very little.

Ex - when this march market took correction 800/1000 points #jindalpoly just consolidating from that time.

Now ready for new high . 💞

🌟Lesson 5 - when market recover the strongest stocks recover very fast & will make new high.

Ex - #happiestmind when market take little correction & again bounce little , then #happiestmind made new high before market .

Ex- #sastasundar after breakout 145/155 zone , stocks in 2/3 weeks given 30/40% return.

And in 2/3 months it was double 💞 https://t.co/9kkc3IV4Lo

I am going to make #priceaction breakout thread with real examples

— V\xb6k\u03c0nT (@Trading0secrets) June 24, 2021

By which u can easily find out blasting stocks.

it is only based on my experience of last 5 years

How many learners are excited \U0001f973

Show your love \u2764 by likes & retweets so that most new one can take advantage.

🌟Lesson 2 - if stock is making same pattern ( in 2 /3hours chart) after given breakout of (weekly /monthly chart) , then chances of stock going up is much more.

Ex - #HGS after given breakout of Trendline ( range) in monthly chart, again making same pattern 4 hours chart. 💞

🌟Lesson 3- if stock never come to retest it's weekly & monthly breakout zone then the chances of it's 2x is much more.

EX - #happiestmind everytime consolidating & making new high. 💞

@chartmojo

@charts_breakout

🌟Lesson 4 - when whole market fall still strongest stocks only consolidate or move down very little.

Ex - when this march market took correction 800/1000 points #jindalpoly just consolidating from that time.

Now ready for new high . 💞

🌟Lesson 5 - when market recover the strongest stocks recover very fast & will make new high.

Ex - #happiestmind when market take little correction & again bounce little , then #happiestmind made new high before market .

1/n

Dear @chartmojo

Out of curiosity, just gone through your timeline and prepared a data of your shared tweets in OCT'2020;

You will not believe the following numbers:

Charts shared = 29 (2 excluded due to splits)

Period = 8-oct to 30-oct'20

..

2/n

If min.10k invested on your each design, then

Amount invested in Oct'20 = 2.91 lacs

Present investment value = 4.72 lacs

Maximum drawdown = 9%

ROI = 62% in 200 days

Annualized ROI = 147%

**You ROCK brother**

...

I've prepared a sheet for all your Oct'20 tweets; It was so much learning on the charts as well as on the data-part; Please keep on the good work.

Sheet link:

https://t.co/8BJtMsOkBD

With regards,

Deepak

Dear @chartmojo

Out of curiosity, just gone through your timeline and prepared a data of your shared tweets in OCT'2020;

You will not believe the following numbers:

Charts shared = 29 (2 excluded due to splits)

Period = 8-oct to 30-oct'20

..

2/n

If min.10k invested on your each design, then

Amount invested in Oct'20 = 2.91 lacs

Present investment value = 4.72 lacs

Maximum drawdown = 9%

ROI = 62% in 200 days

Annualized ROI = 147%

**You ROCK brother**

...

I've prepared a sheet for all your Oct'20 tweets; It was so much learning on the charts as well as on the data-part; Please keep on the good work.

Sheet link:

https://t.co/8BJtMsOkBD

With regards,

Deepak