Categories Finance

7 days

30 days

All time

Recent

Popular

Thread Best books recommendation by one of best investor I knew @insharebazaar (Virtually)

He grab many multibagger stocks and His style also unique(1st Seen interview in @TraderHarneet's YT Channel)

He follow Simple process

Young Intelligent Investor who also appeared in ET

1. One Up On Wall Street

2. Rich Dad Poor Dad

Access here : https://t.co/UWOCF732z6

3. The Unusual Billionaires

4. Trading in the Zone

https://t.co/G7mqVPtEM0

5. Market Wizards

6. The Intelligent Investor

https://t.co/yPKBzYyPAl

7. The Five Rules for Successful Stock Investing

8. Reminiscences of a Stock Operator

https://t.co/PiioB3hdHP

He grab many multibagger stocks and His style also unique(1st Seen interview in @TraderHarneet's YT Channel)

He follow Simple process

Young Intelligent Investor who also appeared in ET

1. One Up On Wall Street

2. Rich Dad Poor Dad

Access here : https://t.co/UWOCF732z6

3. The Unusual Billionaires

4. Trading in the Zone

https://t.co/G7mqVPtEM0

5. Market Wizards

6. The Intelligent Investor

https://t.co/yPKBzYyPAl

7. The Five Rules for Successful Stock Investing

8. Reminiscences of a Stock Operator

https://t.co/PiioB3hdHP

Two year back thread on MFI, someone liked this so came up in notifications . Rather than running around 100s of indicators, I have made this my go to indicator under any circumstances and have been using this for years

This thread actually had some great answers , one can learn a lot about the thought processes of different traders from the answers. Please go thru them

What do you think/use as the most robust leading indicator if following technical analysis ? Please answer with reason , I will provide my answer after 2 hours

— Subhadip Nandy (@SubhadipNandy16) August 12, 2019

( At Delhi airport , bored as hell )

This thread actually had some great answers , one can learn a lot about the thought processes of different traders from the answers. Please go thru them

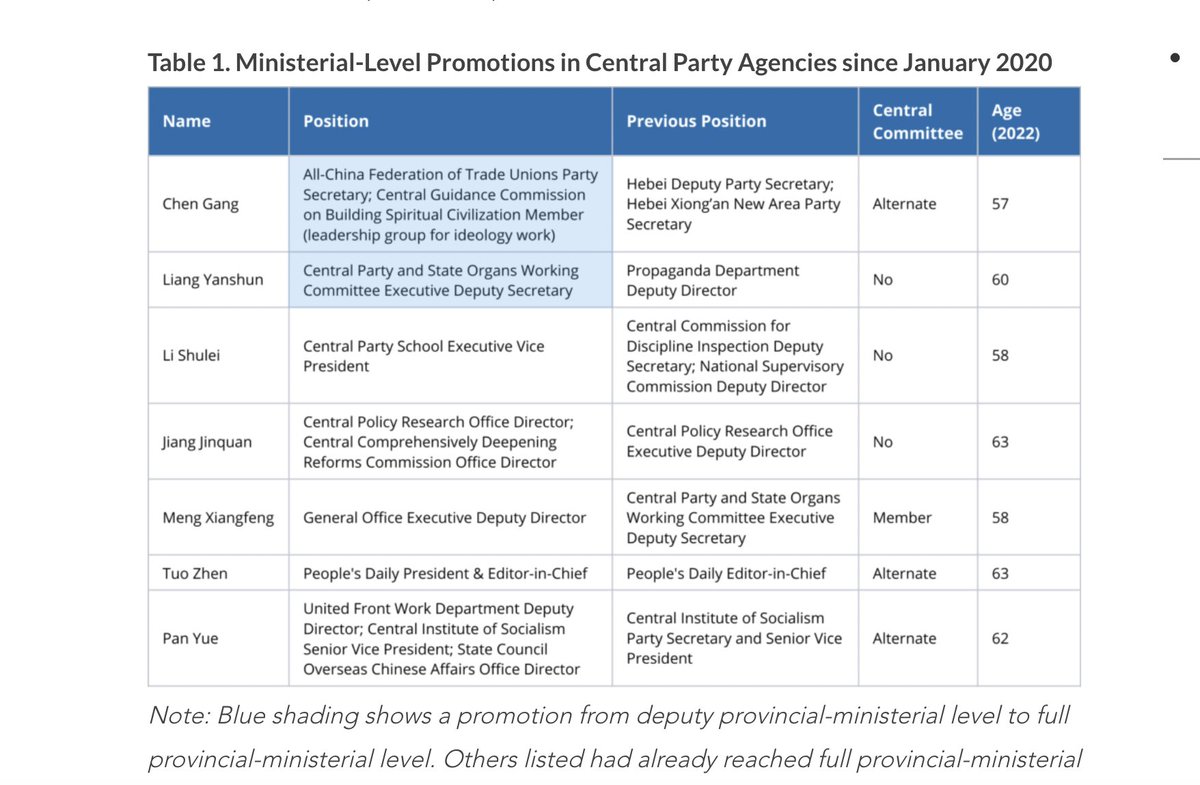

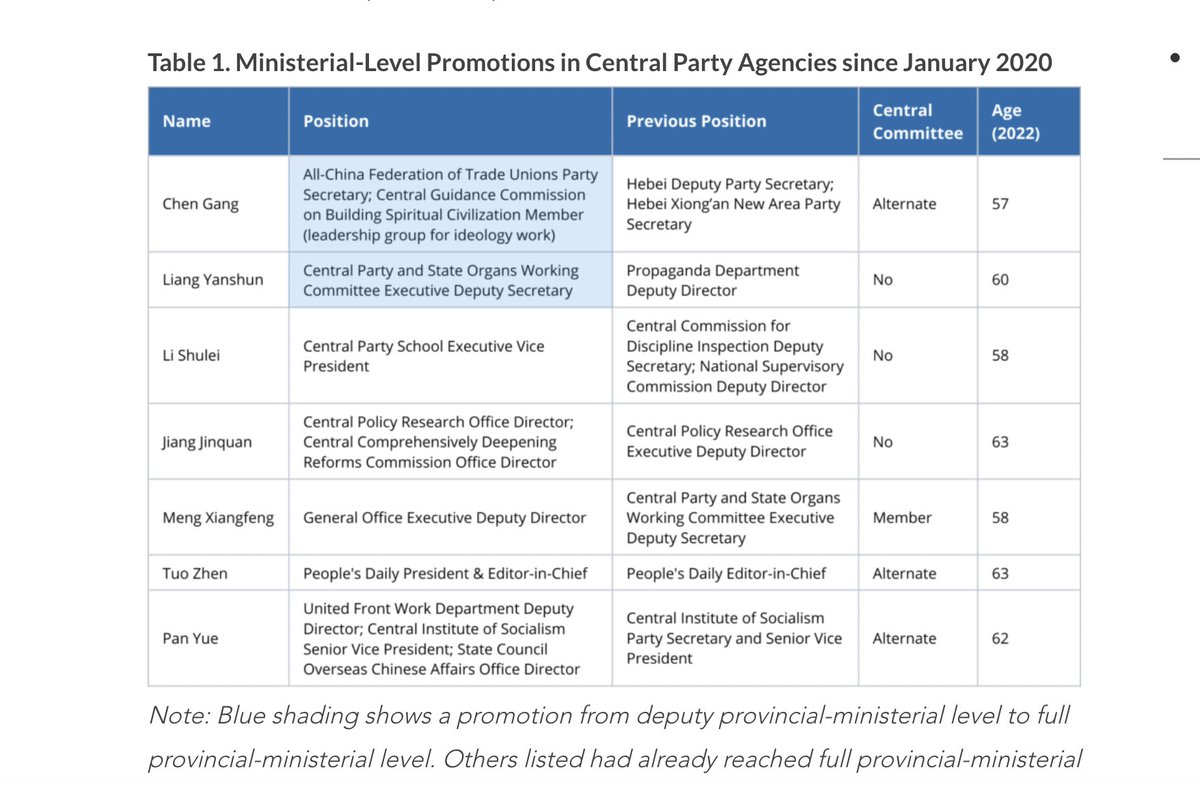

THREAD: Who are the rising stars of Chinese elite politics in the central Party-State bureaucracy?

For @MacroPoloChina I analyzed last year's ministerial-level promotions to posts in Beijing

TLDR: Ties to Xi Jinping—or a Xi ally—are very helpful! (1/14)

https://t.co/kO2A0Efyq2

Seven politicians were promoted to ministerial-level positions in central Party agencies last year

All are likely to feature on the next Central Committee selected at the 2022 Party Congress

Some could make the CCP's elite 25-person Politburo (2/14)

https://t.co/kO2A0Efyq2

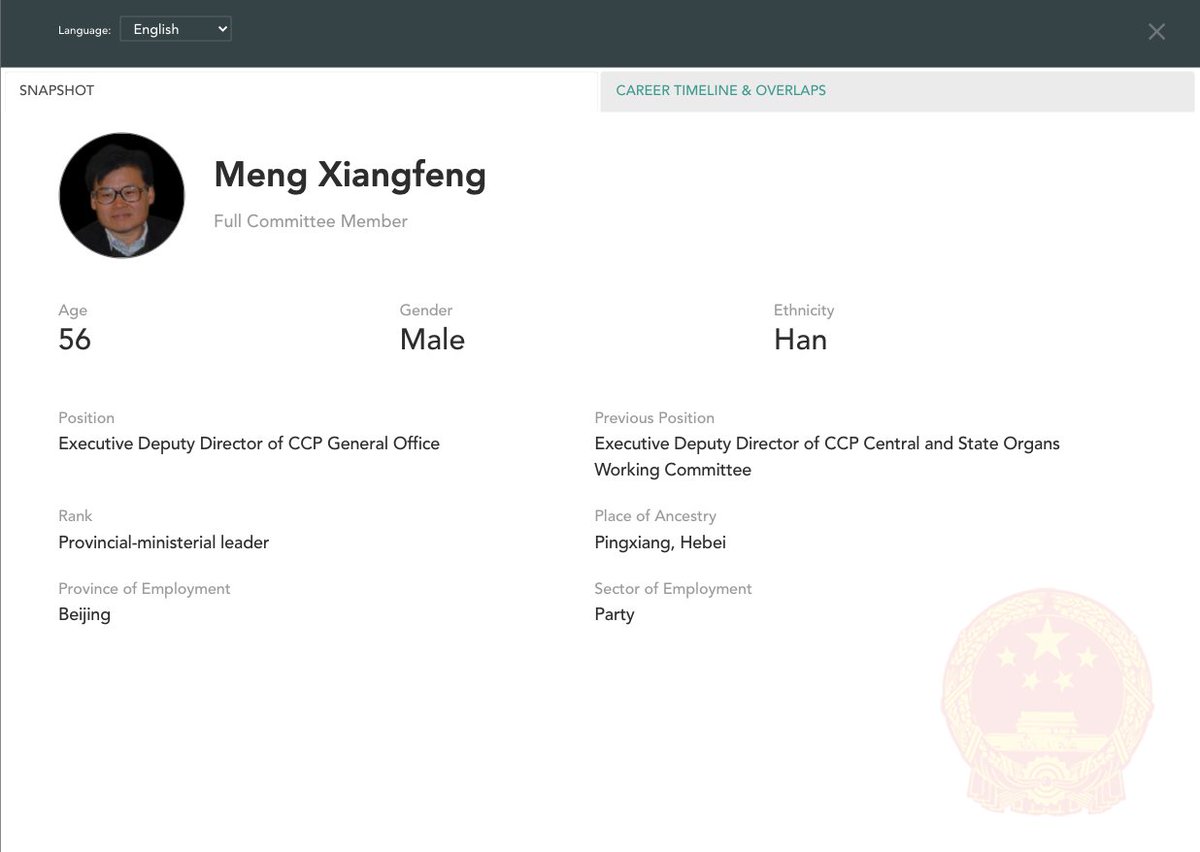

Likeliest for the Politburo is Meng Xiangfeng, new Executive Deputy Director of the CCP General Office

He would replace Xi ally Ding Xuexiang as CCP chief-of-staff if Ding is promoted further in 2022

Meng worked under Xi allies Cai Qi in Hangzhou and Chen Xi in Liaoning (3/14)

Less likely for the Politburo but still important is Jiang Jinquan, new Director of the CCP Policy Research Office

He replaces 5th-ranked leader Wang Huning who led the Party's brains trust for 18 years

Wang remains prominent and will be <68 in 2022, so he'll stay around (4/14)

Other notable central Party promotions include Li Shulei and Liang Yanshun, who both assisted Xi when he led the Central Party School from 2007-2012

Li is a political conservative who is said to be quite close with Xi, even drafting his 2014 speech on culture and art (5/14)

For @MacroPoloChina I analyzed last year's ministerial-level promotions to posts in Beijing

TLDR: Ties to Xi Jinping—or a Xi ally—are very helpful! (1/14)

https://t.co/kO2A0Efyq2

Seven politicians were promoted to ministerial-level positions in central Party agencies last year

All are likely to feature on the next Central Committee selected at the 2022 Party Congress

Some could make the CCP's elite 25-person Politburo (2/14)

https://t.co/kO2A0Efyq2

Likeliest for the Politburo is Meng Xiangfeng, new Executive Deputy Director of the CCP General Office

He would replace Xi ally Ding Xuexiang as CCP chief-of-staff if Ding is promoted further in 2022

Meng worked under Xi allies Cai Qi in Hangzhou and Chen Xi in Liaoning (3/14)

Less likely for the Politburo but still important is Jiang Jinquan, new Director of the CCP Policy Research Office

He replaces 5th-ranked leader Wang Huning who led the Party's brains trust for 18 years

Wang remains prominent and will be <68 in 2022, so he'll stay around (4/14)

Other notable central Party promotions include Li Shulei and Liang Yanshun, who both assisted Xi when he led the Central Party School from 2007-2012

Li is a political conservative who is said to be quite close with Xi, even drafting his 2014 speech on culture and art (5/14)

Ok here is the explanation. Grab a cup of coffee and read on. If you have not read/noticed this, you will see intraday options movement in a new light.

Say we have two options, one 50 delta ATM options and another 30 delta OTM option. Normally for a 100 point move, the ATM option will move 50 points and the OTM option will move 30 points. But in a high volatile environment, the OTM option will also move nearly 50 points

To understand why this happens, first understand why an ATM option is 50 delta. An ATM option has the probability of 50% of expiring as ITM. The price just has to close a rupee above the strike for the CE to be ITM and vice versa for PEs

Now think of a highly volatile day like today. If someone is asked where the BNF will close for the day or expiry, no one can answer. BNF can close freakin anywhere, That makes every option of an equal probability of being ITM. So all options have a 50% probability of being ITM

Hence, when a huge volatile move starts, all OTM options behave like ATM options. This phenomenon was first observed in the Black Monday crash of 1987 at Wall Street, which also gave rise to the volatility skew/smirk

In a high IV environment or when the market is very volatile

— Subhadip Nandy (@SubhadipNandy16) January 21, 2022

" OTM options will behave like ATM options", one will get almost the same delta movement

Say we have two options, one 50 delta ATM options and another 30 delta OTM option. Normally for a 100 point move, the ATM option will move 50 points and the OTM option will move 30 points. But in a high volatile environment, the OTM option will also move nearly 50 points

To understand why this happens, first understand why an ATM option is 50 delta. An ATM option has the probability of 50% of expiring as ITM. The price just has to close a rupee above the strike for the CE to be ITM and vice versa for PEs

Now think of a highly volatile day like today. If someone is asked where the BNF will close for the day or expiry, no one can answer. BNF can close freakin anywhere, That makes every option of an equal probability of being ITM. So all options have a 50% probability of being ITM

Hence, when a huge volatile move starts, all OTM options behave like ATM options. This phenomenon was first observed in the Black Monday crash of 1987 at Wall Street, which also gave rise to the volatility skew/smirk

Today in mezz threads:

Finding collateral where there isn’t any ... aka, my most innovative idea (and I’m giving it to you for free)!

Let’s revisit this thread from my early (active) Twitter days. A few questions you might ask:

1) What was my collateral (why did I make this loan)?

2) Why did I have any leverage with the company at all (short of a foreclosure)?

3) Why did the “deep pockets” buy me out?

Let me pick up the story with two assumptions I had going in:

1) I didn’t trust the owner/operator (at all)

2) I knew the PE group (that had offered $200 M) well, and I knew who they were proposing to bring in to run the company had they bought it

#2 (plan B) made sense to me

The senior ($ZION) had the collateral locked up and controlled any formal foreclosure/bankruptcy.

The idea of a convertible had some appeal but you can’t really do anything with 5-10% of a business

My solution: “default conversion” at an unfair valuation

I negotiated a deal that if the company defaulted (and only if they didn’t cure the defaults) I had the option to convert into preferred stock representing a fully diluted 40% of the business

Finding collateral where there isn’t any ... aka, my most innovative idea (and I’m giving it to you for free)!

Let’s revisit this thread from my early (active) Twitter days. A few questions you might ask:

1) What was my collateral (why did I make this loan)?

2) Why did I have any leverage with the company at all (short of a foreclosure)?

3) Why did the “deep pockets” buy me out?

My typical mezz deals are to companies in 1/3 categories:

— Matt Willes (@SkolCapital) August 27, 2020

1) M&A

2) Growth Capital

3) Special Situations ...

Here\u2019s an example on #3:

Let me pick up the story with two assumptions I had going in:

1) I didn’t trust the owner/operator (at all)

2) I knew the PE group (that had offered $200 M) well, and I knew who they were proposing to bring in to run the company had they bought it

#2 (plan B) made sense to me

The senior ($ZION) had the collateral locked up and controlled any formal foreclosure/bankruptcy.

The idea of a convertible had some appeal but you can’t really do anything with 5-10% of a business

My solution: “default conversion” at an unfair valuation

I negotiated a deal that if the company defaulted (and only if they didn’t cure the defaults) I had the option to convert into preferred stock representing a fully diluted 40% of the business

Buffett's letters taught me more about investing than any business school ever could.

Even after investing for 14 years, I uncover new insights every time I reread his letters.

Recently, I reread his letters from 1977 to 2020 for a third time.

Here are my key insights:

1. Moat is NEVER stagnant

A company's competitive position either grows stronger or weaker each day.

Widening the moat must always take precedence over short-term targets.

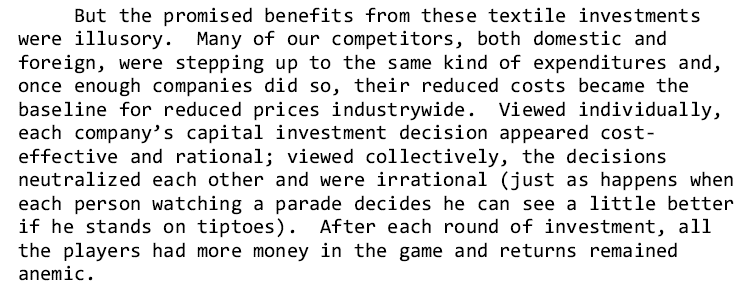

2. Commodity businesses

A business without moat will have its returns competed away.

Regardless of improvement, your competitors will quickly copy your advantage away.

Where returns on capital is dismal, reinvestment will only destroy value.

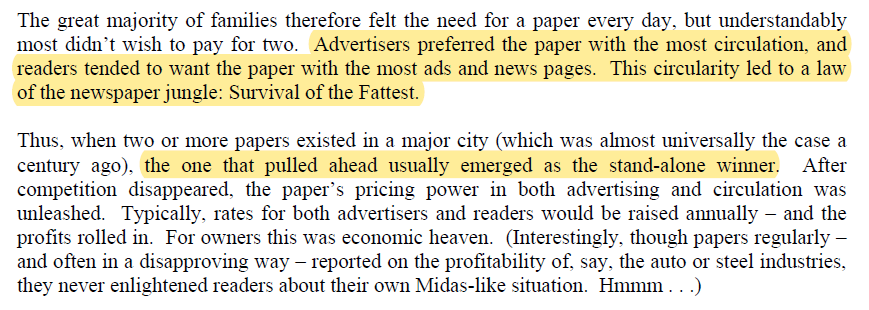

3. The flywheel effect

Buffett was preaching about the flywheel effect before it became cool.

Back then, newspapers were similar to today's platform businesses like Amazon, Meta, and App Store.

More readers beget more advertisers beget more readers.

4. Operating leverage

Companies with high fixed costs and low variable costs will see earnings rise faster than revenue.

However, it cuts both ways.

It becomes a disaster when revenue is declining.

Check out my article on how operating leverage works: https://t.co/Nv747oBAK0

Even after investing for 14 years, I uncover new insights every time I reread his letters.

Recently, I reread his letters from 1977 to 2020 for a third time.

Here are my key insights:

1. Moat is NEVER stagnant

A company's competitive position either grows stronger or weaker each day.

Widening the moat must always take precedence over short-term targets.

2. Commodity businesses

A business without moat will have its returns competed away.

Regardless of improvement, your competitors will quickly copy your advantage away.

Where returns on capital is dismal, reinvestment will only destroy value.

3. The flywheel effect

Buffett was preaching about the flywheel effect before it became cool.

Back then, newspapers were similar to today's platform businesses like Amazon, Meta, and App Store.

More readers beget more advertisers beget more readers.

4. Operating leverage

Companies with high fixed costs and low variable costs will see earnings rise faster than revenue.

However, it cuts both ways.

It becomes a disaster when revenue is declining.

Check out my article on how operating leverage works: https://t.co/Nv747oBAK0

** MEGA THREAD ON Cryptocurrencies/Blockchain**

I wanted to know the best resources to learn about cryptocurrencies and blockchain for someone with zero knowledge. I asked Twitter, and Twitter answered.

This thread is a compilation of the best resources I was recommended. 👇👇

Let's start with ** BOOKS **

The first thing you should do before you pick up any book:

Learn about Bitcoin & Ethereum by reading the respective whitepapers.

- [Bitcoin white paper](https://t.co/cErOaFn6QL) by Satoshi Nakamoto

- [Ethereum White paper] (https://t.co/0g5kYCGJGq) by Vitalik Buterin

Even if you are not tech savvy, you can get a good grasp about how blockchain functions from these papers.

1) *The Basics of Bitcoins and Blockchains: An Introduction to Cryptocurrencies and the Technology that Powers Them* by Antony Lewis

This book covers topics such as the history of Bitcoin, the Bitcoin blockchain, and Bitcoin buying, selling, and mining.

It also answers how payments are made and how transactions are kept secure.

Other cryptocurrencies and cryptocurrency pricing are examined, answering how one puts a value on cryptocurrencies and digital tokens.

I wanted to know the best resources to learn about cryptocurrencies and blockchain for someone with zero knowledge. I asked Twitter, and Twitter answered.

This thread is a compilation of the best resources I was recommended. 👇👇

Let's start with ** BOOKS **

The first thing you should do before you pick up any book:

Learn about Bitcoin & Ethereum by reading the respective whitepapers.

- [Bitcoin white paper](https://t.co/cErOaFn6QL) by Satoshi Nakamoto

- [Ethereum White paper] (https://t.co/0g5kYCGJGq) by Vitalik Buterin

Even if you are not tech savvy, you can get a good grasp about how blockchain functions from these papers.

1) *The Basics of Bitcoins and Blockchains: An Introduction to Cryptocurrencies and the Technology that Powers Them* by Antony Lewis

This book covers topics such as the history of Bitcoin, the Bitcoin blockchain, and Bitcoin buying, selling, and mining.

It also answers how payments are made and how transactions are kept secure.

Other cryptocurrencies and cryptocurrency pricing are examined, answering how one puts a value on cryptocurrencies and digital tokens.

As the DeFi bull market continues, some brutally honest tips for new founders fundraising in crypto.

👇

1/ The discount you offer to strategic investors is both to account for the risk of an unlaunched product, but also as compensation for continued value add and support.

So make sure you know the investor will support you and not leave you on read once the docs are signed!

2/ Having someone on your cap table/ token allocation is as important as hiring.

You wouldn't hire someone just because they are influencers on Twitter- you do your reference checks and find evidence of value add from other companies the investor has invested in.

3/ Don't trust, verify.

Many investors will promise you the world when they're trying to get on your cap table.

Talk to founders they backed to see how much of it is bullshit. Ask them about how the investor was there for them during hard times.

4/ Don't just go for "name brand" funds because you want the brand.

Sure, it's great validation, but optimize for fit, not vanity.

However, I do think many well-known VCs are good actors, especially those with roots in successful trad VCs. They have a rep for a reason!

👇

Equity/ownership is a force. Getting it in the hands of the right people generously will drive alignment and execution.

— Joey Santoro (@Joey__Santoro) January 21, 2021

It is a joyful and serious responsibility \U0001f332

1/ The discount you offer to strategic investors is both to account for the risk of an unlaunched product, but also as compensation for continued value add and support.

So make sure you know the investor will support you and not leave you on read once the docs are signed!

2/ Having someone on your cap table/ token allocation is as important as hiring.

You wouldn't hire someone just because they are influencers on Twitter- you do your reference checks and find evidence of value add from other companies the investor has invested in.

3/ Don't trust, verify.

Many investors will promise you the world when they're trying to get on your cap table.

Talk to founders they backed to see how much of it is bullshit. Ask them about how the investor was there for them during hard times.

4/ Don't just go for "name brand" funds because you want the brand.

Sure, it's great validation, but optimize for fit, not vanity.

However, I do think many well-known VCs are good actors, especially those with roots in successful trad VCs. They have a rep for a reason!