TSMC $TSM projecting capital expenses of 25-28B USD in 2021. 80% allocated for advanced process tech, 3, 5, 7nm. 10% advanced packaging and mask making, 10% other. 2020 capex, originally slated at $15B, was over $17B. For context $AMD's entire revenue for 2020 estimated at $9.5B

All this, especially the capex, in line with suggestions Intel will be increasing their use of TSMC fabs, or else AMD making really large increases (or both), but they also project a lot of growth in phones

I expect some inflation for autos and appliances as production is limited by the silicon shortage. Not like these fabs want to build more capacity at these nodes.

They still plan on continuing to expand in China, but a reset on the leading edge.

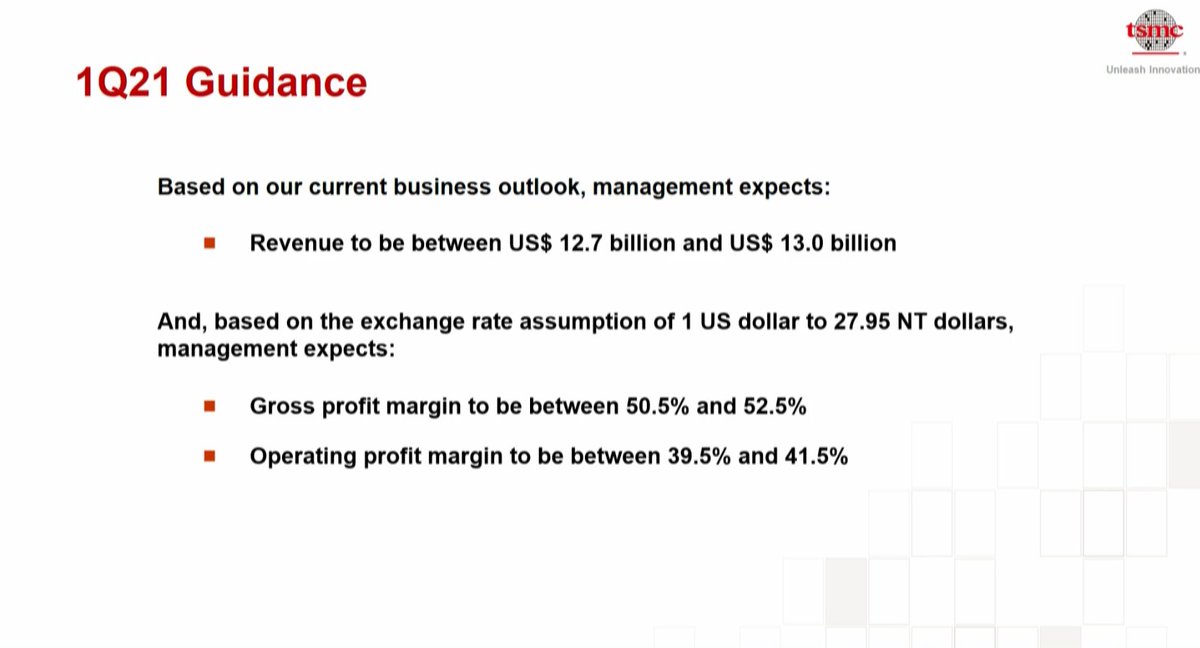

TSMC 4Q earnings remained strong on \u201cextremely high\u201d UTR and some shipments will land 1Q. 1Q21 guided +1% QoQ midpoint, 2021 growing mid-teens USD. Capex up huge $17.2bn to 25-28bn in \u201921, and now expect LT growth of 10-15% CAGR in \u201820-25 vs before 5-10% CAGR....

— cyw60 (@cyw60) January 14, 2021

More from Finance

I'm lucky to attain financial freedom before 30.

I credit Fintwit for my learnings.

Here's 10 key concepts every investor must know:

1. $$ needed to retire

2. Researching a business

3. Reading annual reports

4. Reading earnings calls

5. Criteria of a multi bagger

(Read on...)

6. Holding a multi bagger

7. Economic moats

8. When to buy a stock

9. Earnings vs cashflow

10. Traits of quality companies

Here's my 10 favourite threads on these concepts:

1. How much $$ do you need to retire

Before you start, you must know the end game.

To meet your retirement goals...

How much $$ do you need in your portfolio?

10-K Diver does a good job explaining what's a safe withdrawl rate.

Hint: It's NOT

2. Research a business

Your investment returns are a lagging indicator.

Instead, your research skills are the leading predictor of your results.

Conclusion?

To be a good investor, you must be a great business researcher.

Start with

3. Reading annual reports

This is the bread and butter of a good business analyst.

You cannot just listen to opinions from others.

You must learn to deep dive a business and make your own judgments.

Start with the 10k.

Ming Zhao explains it

I credit Fintwit for my learnings.

Here's 10 key concepts every investor must know:

1. $$ needed to retire

2. Researching a business

3. Reading annual reports

4. Reading earnings calls

5. Criteria of a multi bagger

(Read on...)

6. Holding a multi bagger

7. Economic moats

8. When to buy a stock

9. Earnings vs cashflow

10. Traits of quality companies

Here's my 10 favourite threads on these concepts:

1. How much $$ do you need to retire

Before you start, you must know the end game.

To meet your retirement goals...

How much $$ do you need in your portfolio?

10-K Diver does a good job explaining what's a safe withdrawl rate.

Hint: It's NOT

1/

— 10-K Diver (@10kdiver) July 25, 2020

Get a cup of coffee.

In this thread, I'll help you work out how much money you need to retire.

2. Research a business

Your investment returns are a lagging indicator.

Instead, your research skills are the leading predictor of your results.

Conclusion?

To be a good investor, you must be a great business researcher.

Start with

1/ Thoughts on Research Process

— Mostly Borrowed Ideas (@borrowed_ideas) September 27, 2021

I was invited to present my research process at a college in the US. I am sharing all ten slides here. pic.twitter.com/z0tjZcogfH

3. Reading annual reports

This is the bread and butter of a good business analyst.

You cannot just listen to opinions from others.

You must learn to deep dive a business and make your own judgments.

Start with the 10k.

Ming Zhao explains it

\U0001f9d0How to Read 10Ks Like a Hedge Fund\U0001f9d0

— Ming Zhao (@FabiusMercurius) May 7, 2021

\u201cFundamentals don\u2019t matter anymore!\u201d I\u2019ve heard this a lot lately on Fintwit.\U0001f644

But, for those who\u2019ve diversify beyond $GME and $DOGE, here\u2019s a primer on what metrics fundamental buy-side PMs look at and why:

(real examples outlined)

\U0001f447 pic.twitter.com/tLlNRvpnDK

Buffett's letters taught me more about investing than any business school ever could.

Even after investing for 14 years, I uncover new insights every time I reread his letters.

Recently, I reread his letters from 1977 to 2020 for a third time.

Here are my key insights:

1. Moat is NEVER stagnant

A company's competitive position either grows stronger or weaker each day.

Widening the moat must always take precedence over short-term targets.

2. Commodity businesses

A business without moat will have its returns competed away.

Regardless of improvement, your competitors will quickly copy your advantage away.

Where returns on capital is dismal, reinvestment will only destroy value.

3. The flywheel effect

Buffett was preaching about the flywheel effect before it became cool.

Back then, newspapers were similar to today's platform businesses like Amazon, Meta, and App Store.

More readers beget more advertisers beget more readers.

4. Operating leverage

Companies with high fixed costs and low variable costs will see earnings rise faster than revenue.

However, it cuts both ways.

It becomes a disaster when revenue is declining.

Check out my article on how operating leverage works: https://t.co/Nv747oBAK0

Even after investing for 14 years, I uncover new insights every time I reread his letters.

Recently, I reread his letters from 1977 to 2020 for a third time.

Here are my key insights:

1. Moat is NEVER stagnant

A company's competitive position either grows stronger or weaker each day.

Widening the moat must always take precedence over short-term targets.

2. Commodity businesses

A business without moat will have its returns competed away.

Regardless of improvement, your competitors will quickly copy your advantage away.

Where returns on capital is dismal, reinvestment will only destroy value.

3. The flywheel effect

Buffett was preaching about the flywheel effect before it became cool.

Back then, newspapers were similar to today's platform businesses like Amazon, Meta, and App Store.

More readers beget more advertisers beget more readers.

4. Operating leverage

Companies with high fixed costs and low variable costs will see earnings rise faster than revenue.

However, it cuts both ways.

It becomes a disaster when revenue is declining.

Check out my article on how operating leverage works: https://t.co/Nv747oBAK0