Title VIII: Energy is the key section (page 156 onwards)

▶️ Standard stuff on commitment to competition, unbundling and customer choice

▶️ UK Capacity Market no longer needs to try to integrate overseas Capacity providers & vice versa

(Article ENER.6, Clause 3, page. 160)

2/

▶️ Existing "exemptions" for selected interconnectors will continue to apply.

This means that these interconnectors can continue to sell capacity rights ahead of time, rather than all through close to real-time markets.

(Article ENER.11, page 162)

3/

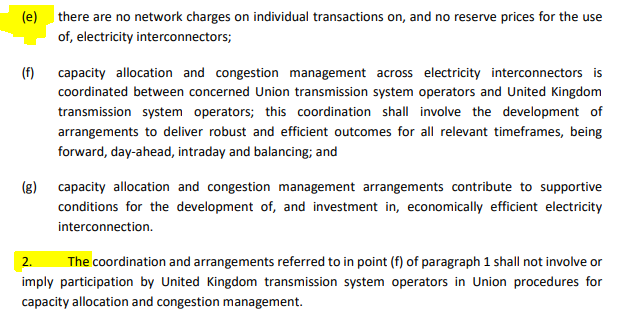

▶️ No network charges on individual interconnector transactions (as now)

▶️ But, UK cannot participate in EU procedures for capacity allocation and congestion management (more on this later)

(Article ENER.13, page 163)

4/

Gas trading: looks like the UK stays in the existing PRISMA gas trading platform.

Not my specialist area, but is this because PRISMA isn't an EU institution (unlike electricity market coupling)?

https://t.co/5GQJtZDpTa (Article ENER. 15, page 164)

5/

▶️ Network development: Parties to cooperate, including on interconnectors, but not much detail.

▶️ Security of Supply: Parties to cooperate, again not much detail. Can't see any references to a solidarity principle.

(Articles ENER. 16 and ENER. 17, page 165)

6/

Cooperation between TSOs & Regulators:

- UK TSOs (i.e. National Grid) to cooperate with EU TSOs through cooperation with ENTSO-E and ENTSOG but not membership

- UK regulator (@Ofgem) to cooperate with EU regulators through ACER. Again, no UK membership

(Articles ENER.19+20)

7/

New cooperation forum between UK and EU on offshore renewable energy.

Looks like UK no longer a member of North Seas Energy Cooperation, so a new forum is needed.

(Article ENER 23, page 169-170).

See summary of our report on Future of North Sea :

https://t.co/Qgh8b2p0yZ 8/

Final provisions, incl. termination (!)

Title on Energy ceases on 30 June 2026. Although can be extended to 31 March 2027 & again to 31 March 2028.

Seems linked to general termination provisions of the deal, including a reference to 🐟🐟 (Article FISH.17)

(ENER 33, p.172)

9/

Onto Annexes. Only Annex ENER-4 is interesting. Covers day-ahead market coupling over interconnectors.

Market coupling ceases on 1 Jan 2021. Will be replaced by April'22 with "Multi-region loose volume coupling"

New term for many

https://t.co/oSVDDiWFw9 Annex ENER-4 p.784

10/

If I understand it correctly, new system will produce net flows on the interconnectors, rather than prices.

Creates a risk that interconnectors flow the "wrong way" (i.e. from high prices to low prices).

Algorithm is separate to EU day-ahead market coupling (EUPHEMIA)

11/

Timeline to develop new system:

▶️ By April 2021: CBA and outline technical proposals

▶️ By November 2021: Technical proposals

▶️ By April 2022: System starts operating

p.785

12/

Other provisions in the deal:

▶️ New Specialised Committee on Energy to discuss/implement some bits of the energy title and annexes (page 12)

▶️ Commitment to carbon pricing in the section on "level playing field"

[Title XI, Article 7.3, page 202]

13/

Overall:

▶️ Lots of sensible provisions, much to gain for both sides

▶️ Market coupling will be weaker, even with new system (Apr 2022)

▶️ Welcome focus on North Sea

▶️ Need to understand more on termination provisions

See more in our recent paper:

https://t.co/KEXNIWvAHJ 14/14