Circle of Competence 101

Warren Buffett and Charlie Munger often reference the importance of knowing the boundaries of your circle of competence.

But what is a Circle of Competence and how does it work?

Here's Circle of Competence 101!

1/ First, a few definitions.

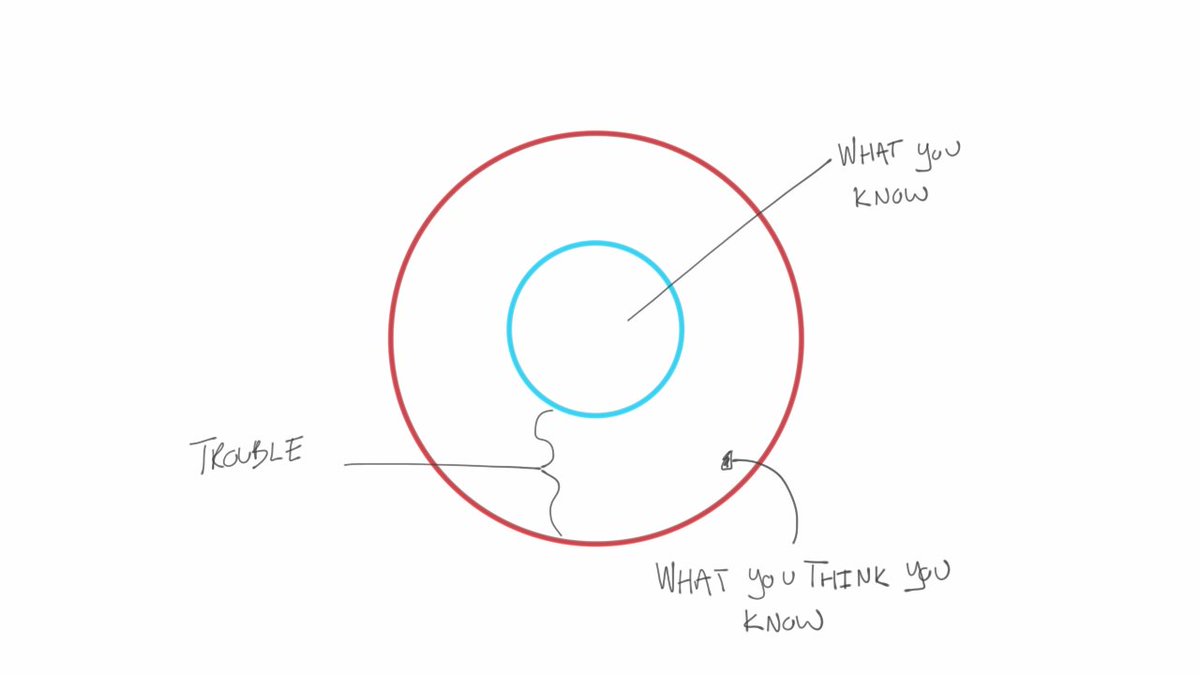

A Circle of Competence is the set of topic areas that align with a person's expertise.

If the entire world of information were to be expressed in a circle, an individual's Circle of Competence is the small sub-circle that represents their expertise.

2/ The idea surfaced in the 1996 BH annual letter.

"You don’t have to be an expert on every company...you only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital."

3/ A Circle of Competence is built over time.

It is built through experience, reading, dedicated study, and effort.

It is dynamic, not static.

It can expand as you deepen your knowledge in new areas. It can contract if you fail to nurture your existing areas of expertise.

4/ To engage this mental model in your life, there are two key processes to go through:

(1) Identify what falls within your circle

(2) Identify the boundaries of your circle

(1) is all about figuring out what you know, while (2) is about humbly admitting what you don’t.