Financial Crisis (1667) avoided by Charles II, via London Goldsmiths' Loans https://t.co/UxtABIpH2n via @old_currency_ex

John Law (baptised 21 April 1671 – 21 March 1729) was a Scottish economist who distinguished money, a means of exchange, from national wealth dependent on trade.

Following Peace of Augsburg, official religion of a territory was determined by "cuius regio, eius religio" The Peace of Westphalia abrogated that principle religion was to be what it had been on 1 January 1624, considered a "normal year".

#NewNormal

More from RealRLD

https://t.co/3XLYTgAnSV via @yumpu_com

#Moduloft The Concept. #Cop26 Draft No.1 Presentation and discussion #BuildBackBetter #LevellingUp

https://t.co/83Lcp66ySk

#Moduloft #AffordableHousingFinance #TheBestMove

Affordable Homes, Are we Looking for a Solution? If so heres where to look!

https://t.co/TFmLjdJWF8 via @yumpu_com Affordable Homes, Are we Looking for a Solution? If so heres where to look! #Moduloft #AffordableHousingFinance #TheBestMove

https://t.co/YUGr2H0HGl

Affordable Homes, Are we Looking for a Solution? If so heres where to look! #Moduloft #AffordableHousingFinance #TheBestMove

https://t.co/qhAB3TOQHo

Affordable Homes, Are we Looking for a Solution? If so heres where to look! #Moduloft #AffordableHousingFinance #TheBestMove

#Moduloft The Concept. #Cop26 Draft No.1 Presentation and discussion #BuildBackBetter #LevellingUp

https://t.co/83Lcp66ySk

#Moduloft #AffordableHousingFinance #TheBestMove

Affordable Homes, Are we Looking for a Solution? If so heres where to look!

https://t.co/TFmLjdJWF8 via @yumpu_com Affordable Homes, Are we Looking for a Solution? If so heres where to look! #Moduloft #AffordableHousingFinance #TheBestMove

https://t.co/YUGr2H0HGl

Affordable Homes, Are we Looking for a Solution? If so heres where to look! #Moduloft #AffordableHousingFinance #TheBestMove

https://t.co/qhAB3TOQHo

Affordable Homes, Are we Looking for a Solution? If so heres where to look! #Moduloft #AffordableHousingFinance #TheBestMove

More from Finance

Thread: P&F Super Pattern

An effective price pattern defined using properties of P&F charts.

#Superpattern #Pointandfigure #Definedge

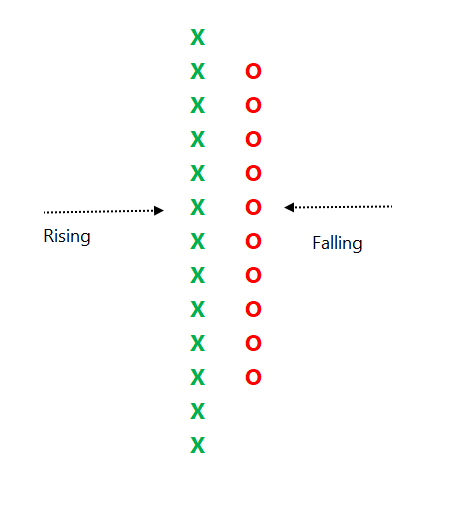

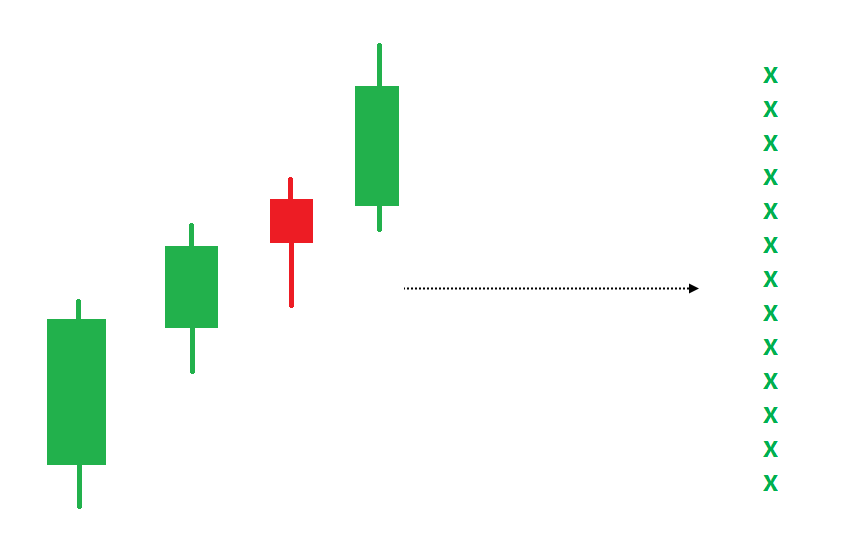

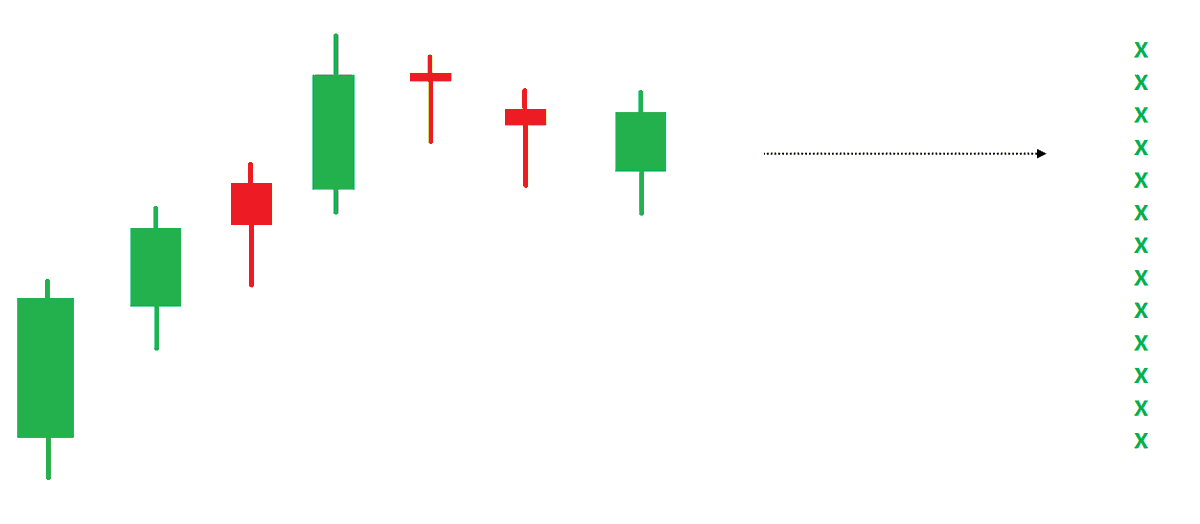

Point & Figure is an oldest charting method where price is plotted vertically, and the chart moves only when price moves. It is a different way of looking at the price, the objective box-value and reversal value offers advantage of identifying objective price patterns.

When price is moving up, it is plotted in a column of 'X'. When it is going down, it is plotted in a column of ‘O’. Normally, three-box reversal criteria is used to define the trend & reversal. Unlike a bar or candle, the P&F column can have multiple sessions in it.

Link to know more about the subject:

https://t.co/2xtLAVPBvm

See below chart. Price is in a strong uptrend, P&F chart would produce a long of column of 'X' with more number of boxes in it.

If such a trend is followed by some time bars without meaningful price correct, P&F chart would not move, and it will remain in column of 'X' in such a scenario.

An effective price pattern defined using properties of P&F charts.

#Superpattern #Pointandfigure #Definedge

Point & Figure is an oldest charting method where price is plotted vertically, and the chart moves only when price moves. It is a different way of looking at the price, the objective box-value and reversal value offers advantage of identifying objective price patterns.

When price is moving up, it is plotted in a column of 'X'. When it is going down, it is plotted in a column of ‘O’. Normally, three-box reversal criteria is used to define the trend & reversal. Unlike a bar or candle, the P&F column can have multiple sessions in it.

Link to know more about the subject:

https://t.co/2xtLAVPBvm

See below chart. Price is in a strong uptrend, P&F chart would produce a long of column of 'X' with more number of boxes in it.

If such a trend is followed by some time bars without meaningful price correct, P&F chart would not move, and it will remain in column of 'X' in such a scenario.

You May Also Like

1/Politics thread time.

To me, the most important aspect of the 2018 midterms wasn't even about partisan control, but about democracy and voting rights. That's the real battle.

2/The good news: It's now an issue that everyone's talking about, and that everyone cares about.

3/More good news: Florida's proposition to give felons voting rights won. But it didn't just win - it won with substantial support from Republican voters.

That suggests there is still SOME grassroots support for democracy that transcends

4/Yet more good news: Michigan made it easier to vote. Again, by plebiscite, showing broad support for voting rights as an

5/OK, now the bad news.

We seem to have accepted electoral dysfunction in Florida as a permanent thing. The 2000 election has never really

To me, the most important aspect of the 2018 midterms wasn't even about partisan control, but about democracy and voting rights. That's the real battle.

2/The good news: It's now an issue that everyone's talking about, and that everyone cares about.

3/More good news: Florida's proposition to give felons voting rights won. But it didn't just win - it won with substantial support from Republican voters.

That suggests there is still SOME grassroots support for democracy that transcends

4/Yet more good news: Michigan made it easier to vote. Again, by plebiscite, showing broad support for voting rights as an

5/OK, now the bad news.

We seem to have accepted electoral dysfunction in Florida as a permanent thing. The 2000 election has never really

Bad ballot design led to a lot of undervotes for Bill Nelson in Broward Co., possibly even enough to cost him his Senate seat. They do appear to be real undervotes, though, instead of tabulation errors. He doesn't really seem to have a path to victory. https://t.co/utUhY2KTaR

— Nate Silver (@NateSilver538) November 16, 2018

I'm going to do two history threads on Ethiopia, one on its ancient history, one on its modern story (1800 to today). 🇪🇹

I'll begin with the ancient history ... and it goes way back. Because modern humans - and before that, the ancestors of humans - almost certainly originated in Ethiopia. 🇪🇹 (sub-thread):

The first likely historical reference to Ethiopia is ancient Egyptian records of trade expeditions to the "Land of Punt" in search of gold, ebony, ivory, incense, and wild animals, starting in c 2500 BC 🇪🇹

Ethiopians themselves believe that the Queen of Sheba, who visited Israel's King Solomon in the Bible (c 950 BC), came from Ethiopia (not Yemen, as others believe). Here she is meeting Solomon in a stain-glassed window in Addis Ababa's Holy Trinity Church. 🇪🇹

References to the Queen of Sheba are everywhere in Ethiopia. The national airline's frequent flier miles are even called "ShebaMiles". 🇪🇹

I'll begin with the ancient history ... and it goes way back. Because modern humans - and before that, the ancestors of humans - almost certainly originated in Ethiopia. 🇪🇹 (sub-thread):

The famous \u201cLucy\u201d, an early ancestor of modern humans (Australopithecus) that lived 3.2 million years ago, and was discovered in 1974 in Ethiopia, displayed in the national museum in Addis Ababa \U0001f1ea\U0001f1f9 pic.twitter.com/N3oWqk1SW2

— Patrick Chovanec (@prchovanec) November 9, 2018

The first likely historical reference to Ethiopia is ancient Egyptian records of trade expeditions to the "Land of Punt" in search of gold, ebony, ivory, incense, and wild animals, starting in c 2500 BC 🇪🇹

Ethiopians themselves believe that the Queen of Sheba, who visited Israel's King Solomon in the Bible (c 950 BC), came from Ethiopia (not Yemen, as others believe). Here she is meeting Solomon in a stain-glassed window in Addis Ababa's Holy Trinity Church. 🇪🇹

References to the Queen of Sheba are everywhere in Ethiopia. The national airline's frequent flier miles are even called "ShebaMiles". 🇪🇹