Categories Crypto

7 days

30 days

All time

Recent

Popular

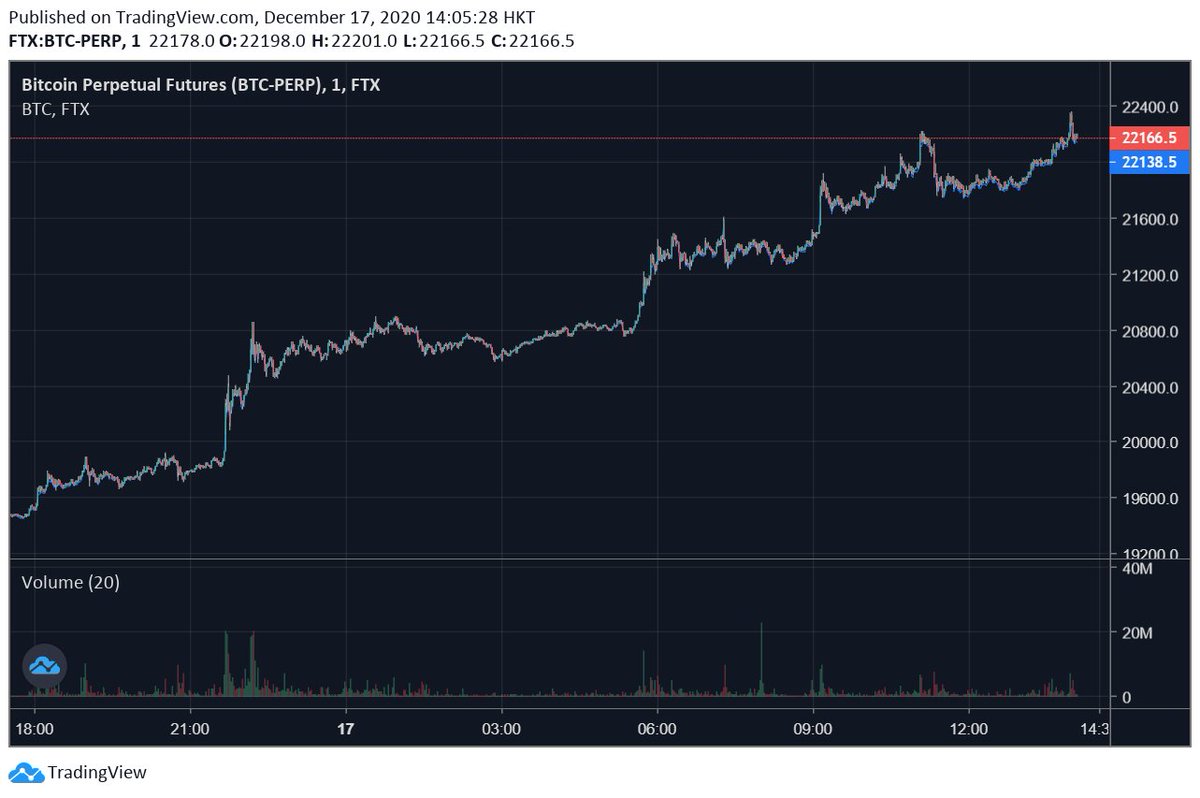

Many close calls later, BTC finally managed to break through $20k -- and it BLEW through it, barely slowing down til $22k. What was different this time?

A thread about man vs. machine.

https://t.co/mGRJ852xVb

As has been pointed out, I've been adamant that the rallies in the past month or so have been heavily fueled by rampant liquidations on both BitMEX and Binance. And they have! But they were also fueled by organic buying among U.S. investors, as has been a popular narrative.

If anything, the narratives surrounding various U.S. funds and other companies buying BTC have gotten *stronger* in the past week or two than they were around Thanksgiving. More and more funds have announced their crypto holdings or plans to acquire them.

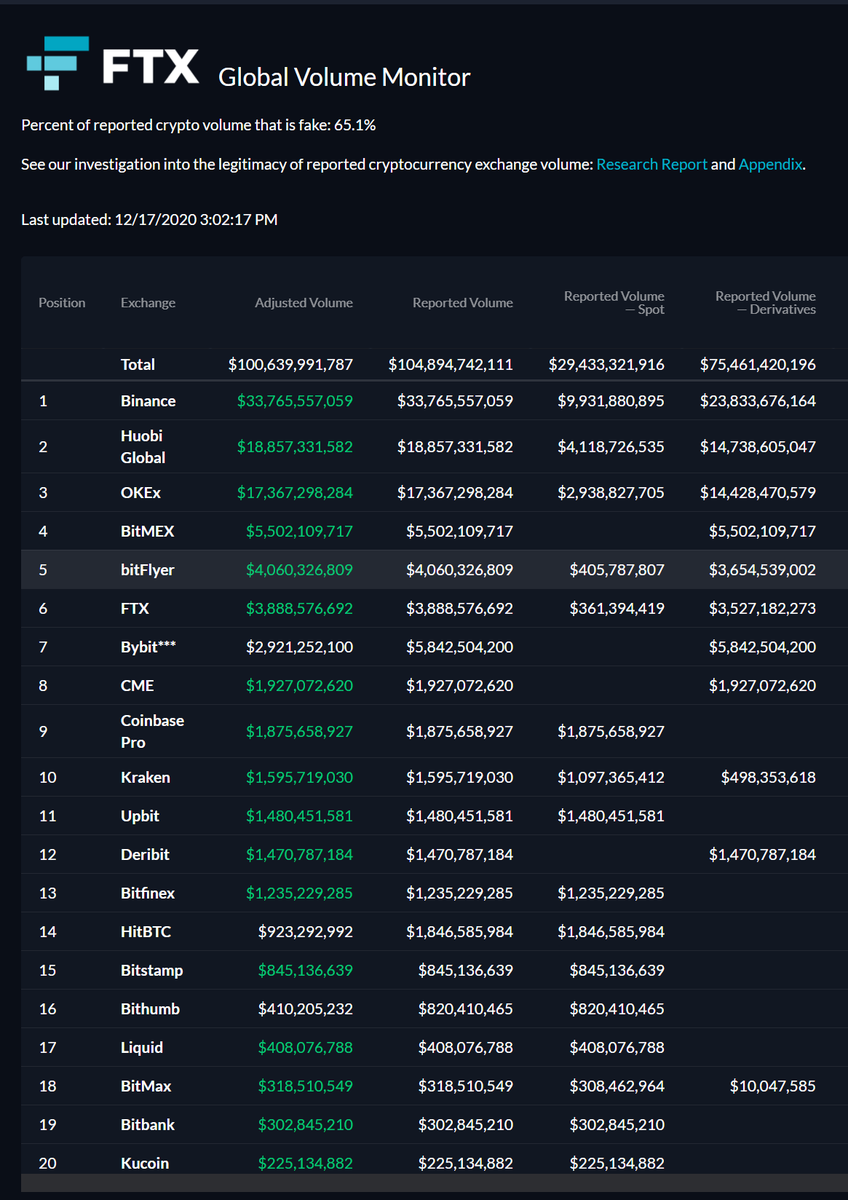

And direct signs of all this exist. Take a look at FTX's volume monitor: U.S. trading hubs like Coinbase having more volume than normal *is* a signal that U.S. customers are doing *something*, and when BTC is going up ...

(Coinbase even crashed from "heightened activity :P).

The DOW recently announced their new crypto indices, CME is listing ETH futures, Microstrategy putting $650M into BTC, GBTC AUM continuing to balloon, these all point in the same direction, and that direction is a resounding "up" for the crypto markets.

A thread about man vs. machine.

https://t.co/mGRJ852xVb

Alameda won't be participating in this, but it does present a chance to explain how we think about the value of man vs. machine in our trading. https://t.co/62yGWAS1C3

— Sam Trabucco (@AlamedaTrabucco) May 26, 2020

As has been pointed out, I've been adamant that the rallies in the past month or so have been heavily fueled by rampant liquidations on both BitMEX and Binance. And they have! But they were also fueled by organic buying among U.S. investors, as has been a popular narrative.

If anything, the narratives surrounding various U.S. funds and other companies buying BTC have gotten *stronger* in the past week or two than they were around Thanksgiving. More and more funds have announced their crypto holdings or plans to acquire them.

And direct signs of all this exist. Take a look at FTX's volume monitor: U.S. trading hubs like Coinbase having more volume than normal *is* a signal that U.S. customers are doing *something*, and when BTC is going up ...

(Coinbase even crashed from "heightened activity :P).

The DOW recently announced their new crypto indices, CME is listing ETH futures, Microstrategy putting $650M into BTC, GBTC AUM continuing to balloon, these all point in the same direction, and that direction is a resounding "up" for the crypto markets.

The Nakamoto Collective is almost the only forward looking thing I can think of. 11 years ago, I was unable to get our Prime Broker to take seriously that a small Hedge Fund wanted to speculate on some new concept. It was so cumbersome that I gave up and wrote an essay instead...

I remember the polite discussion about liquidity, clearing, custody, spreads, etc. By the end, they were laughing at us. There is something about *institutional* ridicule that allows those who had just blown up the world to deride others even when the institutions are disgraced.

Bitcoin at the time felt totally sketchy as a financial instrument as it was tied to contraband. But I didn’t see it as money. If I did, I would be unimaginably wealthy if I didn’t lose it all to digital theft, accidental loss or spending it . But I am an idiot in these matters.

The reason I was interested in it was more complex. If Bitcoin was digital gold, and gold was a quantum mechanical wave, then some group had created a:

1) Novel

2) Locally enforced

3) Digital

4) Conservation law

Called the blockchain. And money was but one thing it could be.

Can you imagine. Some group was creating as-if physics inside the network. Bitcoins to me were ‘waves’ propagating not in vector bundles, but on networked computers as substrate.

This was genius. I reasoned at the time that it didn’t make sense to me as a medium of exchange.

On #Bitcoin\u2018s 12th birthday, Satoshi Nakamoto just became the 40th richest person in the world.

— Ryan Watkins (@RyanWatkins_) January 3, 2021

$34 billion and counting \U0001f680 pic.twitter.com/hIE0he9O93

I remember the polite discussion about liquidity, clearing, custody, spreads, etc. By the end, they were laughing at us. There is something about *institutional* ridicule that allows those who had just blown up the world to deride others even when the institutions are disgraced.

Bitcoin at the time felt totally sketchy as a financial instrument as it was tied to contraband. But I didn’t see it as money. If I did, I would be unimaginably wealthy if I didn’t lose it all to digital theft, accidental loss or spending it . But I am an idiot in these matters.

The reason I was interested in it was more complex. If Bitcoin was digital gold, and gold was a quantum mechanical wave, then some group had created a:

1) Novel

2) Locally enforced

3) Digital

4) Conservation law

Called the blockchain. And money was but one thing it could be.

Can you imagine. Some group was creating as-if physics inside the network. Bitcoins to me were ‘waves’ propagating not in vector bundles, but on networked computers as substrate.

This was genius. I reasoned at the time that it didn’t make sense to me as a medium of exchange.

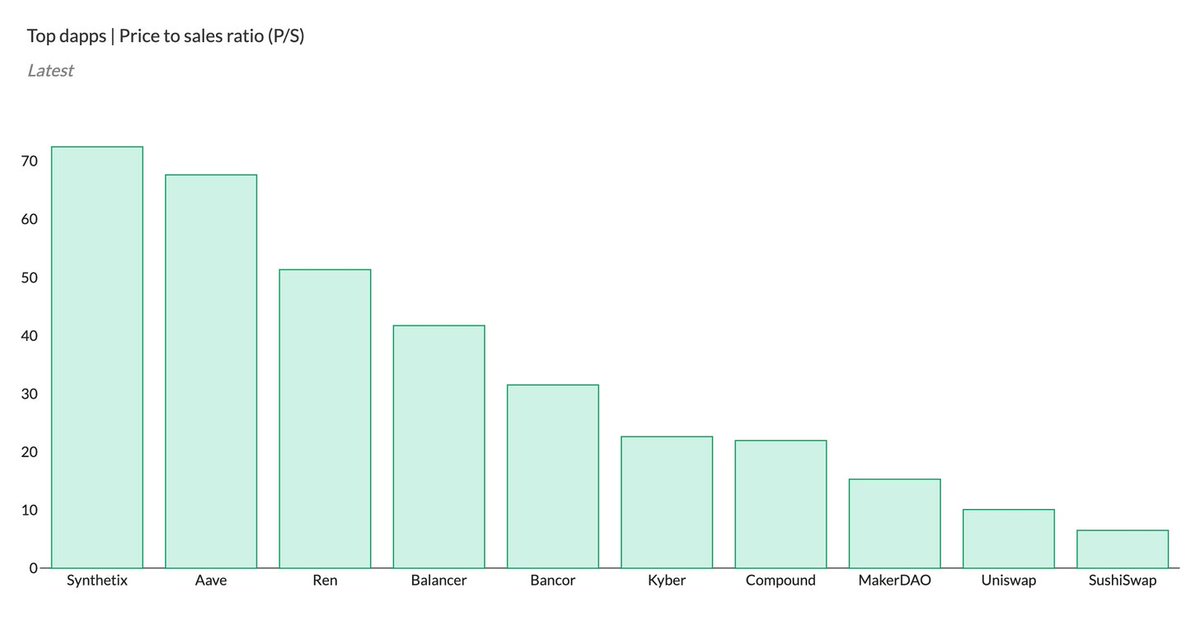

1/ Why the price to sales ratio (P/S) is a useful tool for crypto investors 👇

The price to sales ratio compares a protocol’s market cap to its revenues. A low ratio could imply that the protocol is undervalued and vice versa.

2/ The P/S ratio is an ideal valuation method for early-stage protocols, which often have little or no net income.

Instead, the P/S ratio focuses on the usage of a protocol, by tracking the total fees paid (revenue) by the users of its service. More info: https://t.co/XlHI7XPTvI

3/ We’re in a historically unique position, with early-stage & high-growth startups operating transparently on-chain.

This transparency makes it possible to find protocols with high usage relative to market cap.

4/ Top dapps from Token Terminal sorted based on the price to sales (P/S) ratio.

Note: Maker has gone from a high P/S ratio to #3 in a matter of months after raising the stability fees for DAI.

Also, two currently similar AMMs (Uniswap & SushiSwap) have the lowest P/S ratios.

5/ Let's look at the P/S ratios from a historical perspective.

The P/S ratio is calculated by dividing a project’s fully-diluted market cap by its annualized revenues.

The metric itself does not tell us about the growth patterns in a protocol’s market cap or revenues.

The price to sales ratio compares a protocol’s market cap to its revenues. A low ratio could imply that the protocol is undervalued and vice versa.

2/ The P/S ratio is an ideal valuation method for early-stage protocols, which often have little or no net income.

Instead, the P/S ratio focuses on the usage of a protocol, by tracking the total fees paid (revenue) by the users of its service. More info: https://t.co/XlHI7XPTvI

3/ We’re in a historically unique position, with early-stage & high-growth startups operating transparently on-chain.

This transparency makes it possible to find protocols with high usage relative to market cap.

4/ Top dapps from Token Terminal sorted based on the price to sales (P/S) ratio.

Note: Maker has gone from a high P/S ratio to #3 in a matter of months after raising the stability fees for DAI.

Also, two currently similar AMMs (Uniswap & SushiSwap) have the lowest P/S ratios.

5/ Let's look at the P/S ratios from a historical perspective.

The P/S ratio is calculated by dividing a project’s fully-diluted market cap by its annualized revenues.

The metric itself does not tell us about the growth patterns in a protocol’s market cap or revenues.

1) Our thoughts on LTO Network

Not financial advice

2) Overview

- LTO Network (https://t.co/LJUDzLMCb5) is a hybrid blockchain solution that connects to existing systems enabling efficient collaboration on complex and multi stakeholder processes. It is led by a great team of serial entrepreneurs.

3) - In other words, LTO gives institutions access to blockchain without requiring them to overhaul legacy systems.

- Businesses don’t want an IT overhaul, but want communication with existing systems that only share process data and updates users via their own systems.

4) - This is the power of LTO network – changing unstructured communications into structured communications and driving efficiency for traditional businesses and institutions.

5) - On December 17, 2020 LTO Network and VIDT Datalink merged sales, marketing and development resources to form a “larger organization…better positioned to serve multinationals around the globe…”

Not financial advice

2) Overview

- LTO Network (https://t.co/LJUDzLMCb5) is a hybrid blockchain solution that connects to existing systems enabling efficient collaboration on complex and multi stakeholder processes. It is led by a great team of serial entrepreneurs.

3) - In other words, LTO gives institutions access to blockchain without requiring them to overhaul legacy systems.

- Businesses don’t want an IT overhaul, but want communication with existing systems that only share process data and updates users via their own systems.

4) - This is the power of LTO network – changing unstructured communications into structured communications and driving efficiency for traditional businesses and institutions.

5) - On December 17, 2020 LTO Network and VIDT Datalink merged sales, marketing and development resources to form a “larger organization…better positioned to serve multinationals around the globe…”

Our CEO discovered #Bitcoin in 2009 on @HackerNews and became quickly fascinated by it through his interests in peer-to-peer technologies and finance. He started trading #Bitcoins in 2010 and implemented his own #Bitcoin client not much later to understand the protocol in detail

Since then, he has been following it for more than 10-years through three distinct periods he calls; “Ealy stages (2009–2013)”, “Becoming Mainstream (2014–2017)”, and “#Altcoin Explosion (2018 -2020)”

Although the value of #Bitcoin and other #Cryptos have increased, they did not become as successful as he thought they could...

The technology behind #Bitcoin, #Blockchain, is a great #innovation but has some significant issues. Below, we provide our CEO’s analysis of these issues across 3 categories; https://t.co/7OTtWyDep9 2.Governance and 3.Scalability

The lack of #security in #Blockchains is almost there by design: a hack, a password loss, or hard disk crash is permanent, and the transaction cannot be reversed. You need to make backups, but not too many and you can never really trust a third-party with them...

Since then, he has been following it for more than 10-years through three distinct periods he calls; “Ealy stages (2009–2013)”, “Becoming Mainstream (2014–2017)”, and “#Altcoin Explosion (2018 -2020)”

Although the value of #Bitcoin and other #Cryptos have increased, they did not become as successful as he thought they could...

The technology behind #Bitcoin, #Blockchain, is a great #innovation but has some significant issues. Below, we provide our CEO’s analysis of these issues across 3 categories; https://t.co/7OTtWyDep9 2.Governance and 3.Scalability

The lack of #security in #Blockchains is almost there by design: a hack, a password loss, or hard disk crash is permanent, and the transaction cannot be reversed. You need to make backups, but not too many and you can never really trust a third-party with them...