Money is its raw material.

#idfcfirstbank is my largest and oldest investment. Thought of creating a thread to explain the business. If you like the thread, please spread the knowledge, retweet. Buckle up, because this is going to be a long one. :D

Money is its raw material.

Let’s understand how a bank makes profits.

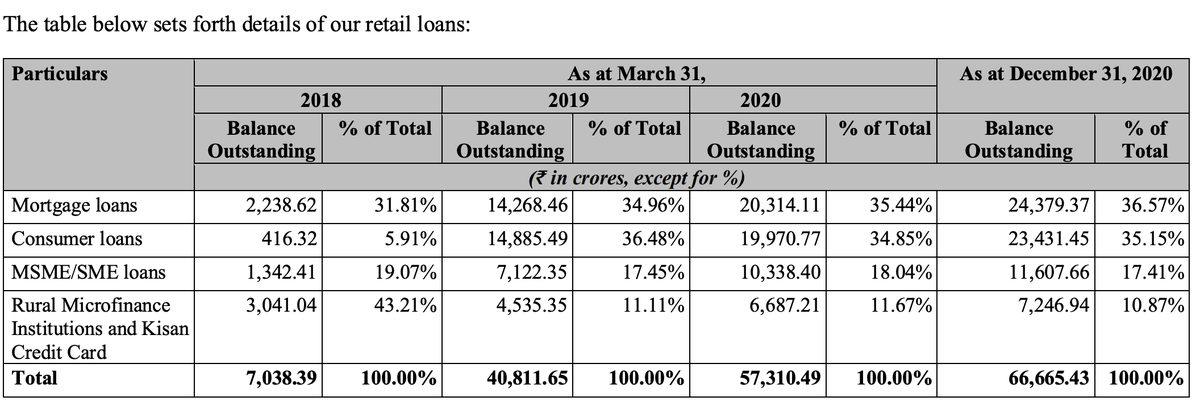

Here are the types of loans that the bank offers. Pay special attention to the very first tile. We will come back to this later.

Reduction in credit to first time borrowers, and increase in credit to customers with high credit scores.

Pre-covid, bank’s GNPA was around 2.6%. Post covid, it has risen to ~4.1%. I personally think this is a great performance given that a large part of the book is lending to SME and Micro Finance.

The Net Interest Income (NII, https://t.co/uKviEG5zGU) for the bank was Rs 10,000 cr for FY21. But profits only Rs 450 cr. Why? Coz profits got eaten by up CIR and provisions.

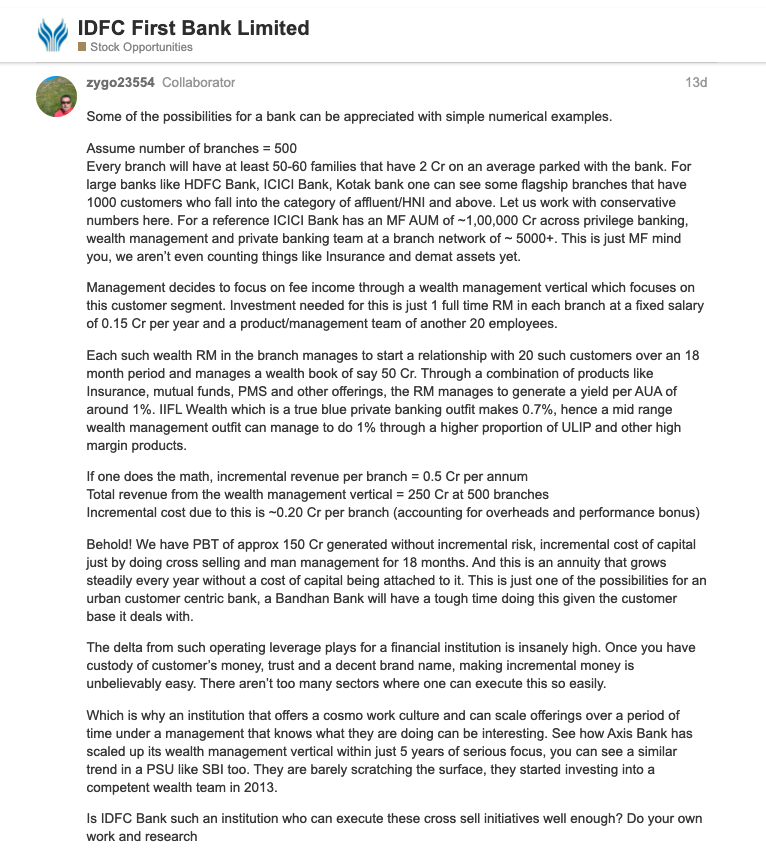

https://t.co/YtYagUR8KC. The cross selling opportunity has only started.

https://t.co/NVxwhgOTaK

1. If bank does not follow conservative underwriting processes, NPAs could blow up and eat into NIMs.

3. Any covid wave would cause short term pain to the bank’s lendees.

More from Sahil Sharma

Such opportunities only come once in a few years.

Step-by-step: how to use (the free) @screener_in to generate investment ideas.

Do retweet if you find it useful to benefit max investors. 🙏🙏

Ready or not, 🧵🧵⤵️

I will use the free screener version so that everyone can follow along.

Outline

1. Stepwise Guide

2. Practical Example: CoffeeCan Companies

3. Practical Example: Smallcap Consistent compounders

4. Practical Example: Smallcap turnaround

5. Key Takeaway

1. Stepwise Guide

Step1

Go to https://t.co/jtOL2Bpoys

Step2

Go to "SCREENS" tab

Step3

Go to "CREATE NEW SCREEN"

At this point you need to register. No charges. I did that with my brother's email id. This is what you see after that.

Step-by-step: how to use (the free) @screener_in to generate investment ideas.

Do retweet if you find it useful to benefit max investors. 🙏🙏

Ready or not, 🧵🧵⤵️

I will use the free screener version so that everyone can follow along.

Outline

1. Stepwise Guide

2. Practical Example: CoffeeCan Companies

3. Practical Example: Smallcap Consistent compounders

4. Practical Example: Smallcap turnaround

5. Key Takeaway

1. Stepwise Guide

Step1

Go to https://t.co/jtOL2Bpoys

Step2

Go to "SCREENS" tab

Step3

Go to "CREATE NEW SCREEN"

At this point you need to register. No charges. I did that with my brother's email id. This is what you see after that.

Most of market does not beat the market by a lot. Which is alright.

In any activity the distribution of outcomes follows bell curve (Gaussian).

Those that are willing to put in effort reap the benefits. 😀

Otherwise we always have option to go for hard working PM's/etf/mf

For lot of consumer facing cos scuttlebutt is actually not that hard. We find reviews online (eg: app reviews on playstore, or reviews of products on social media)

B2B is hard to scuttlebutt, need to reach out to people in co and hope that are willing to talk. Connections help

In any activity the distribution of outcomes follows bell curve (Gaussian).

Those that are willing to put in effort reap the benefits. 😀

Otherwise we always have option to go for hard working PM's/etf/mf

Things to need to do before you buy a stock. I wonder though how many investors have the ability for item numbers 5, 6 & 7. I don't pic.twitter.com/E5AMVxbpNb

— Prashanth (@Prashanth_Krish) August 16, 2021

For lot of consumer facing cos scuttlebutt is actually not that hard. We find reviews online (eg: app reviews on playstore, or reviews of products on social media)

B2B is hard to scuttlebutt, need to reach out to people in co and hope that are willing to talk. Connections help

More from All

MASTER THREAD on Short Strangles.

Curated the best tweets from the best traders who are exceptional at managing strangles.

• Positional Strangles

• Intraday Strangles

• Position Sizing

• How to do Adjustments

• Plenty of Examples

• When to avoid

• Exit Criteria

How to sell Strangles in weekly expiry as explained by boss himself. @Mitesh_Engr

• When to sell

• How to do Adjustments

• Exit

Beautiful explanation on positional option selling by @Mitesh_Engr

Sir on how to sell low premium strangles yourself without paying anyone. This is a free mini course in

1st Live example of managing a strangle by Mitesh Sir. @Mitesh_Engr

• Sold Strangles 20% cap used

• Added 20% cap more when in profit

• Booked profitable leg and rolled up

• Kept rolling up profitable leg

• Booked loss in calls

• Sold only

2nd example by @Mitesh_Engr Sir on converting a directional trade into strangles. Option Sellers can use this for consistent profit.

• Identified a reversal and sold puts

• Puts decayed a lot

• When achieved 2% profit through puts then sold

Curated the best tweets from the best traders who are exceptional at managing strangles.

• Positional Strangles

• Intraday Strangles

• Position Sizing

• How to do Adjustments

• Plenty of Examples

• When to avoid

• Exit Criteria

How to sell Strangles in weekly expiry as explained by boss himself. @Mitesh_Engr

• When to sell

• How to do Adjustments

• Exit

1. Let's start option selling learning.

— Mitesh Patel (@Mitesh_Engr) February 10, 2019

Strangle selling. ( I am doing mostly in weekly Bank Nifty)

When to sell? When VIX is below 15

Assume spot is at 27500

Sell 27100 PE & 27900 CE

say premium for both 50-50

If bank nifty will move in narrow range u will get profit from both.

Beautiful explanation on positional option selling by @Mitesh_Engr

Sir on how to sell low premium strangles yourself without paying anyone. This is a free mini course in

Few are selling 20-25 Rs positional option selling course.

— Mitesh Patel (@Mitesh_Engr) November 3, 2019

Nothing big deal in that.

For selling weekly option just identify last week low and high.

Now from that low and high keep 1-1.5% distance from strike.

And sell option on both side.

1/n

1st Live example of managing a strangle by Mitesh Sir. @Mitesh_Engr

• Sold Strangles 20% cap used

• Added 20% cap more when in profit

• Booked profitable leg and rolled up

• Kept rolling up profitable leg

• Booked loss in calls

• Sold only

Sold 29200 put and 30500 call

— Mitesh Patel (@Mitesh_Engr) April 12, 2019

Used 20% capital@44 each

2nd example by @Mitesh_Engr Sir on converting a directional trade into strangles. Option Sellers can use this for consistent profit.

• Identified a reversal and sold puts

• Puts decayed a lot

• When achieved 2% profit through puts then sold

Already giving more than 2% return in a week. Now I will prefer to sell 32500 call at 74 to make it strangle in equal ratio.

— Mitesh Patel (@Mitesh_Engr) February 7, 2020

To all. This is free learning for you. How to play option to make consistent return.

Stay tuned and learn it here free of cost. https://t.co/7J7LC86oW0

How can we use language supervision to learn better visual representations for robotics?

Introducing Voltron: Language-Driven Representation Learning for Robotics!

Paper: https://t.co/gIsRPtSjKz

Models: https://t.co/NOB3cpATYG

Evaluation: https://t.co/aOzQu95J8z

🧵👇(1 / 12)

Videos of humans performing everyday tasks (Something-Something-v2, Ego4D) offer a rich and diverse resource for learning representations for robotic manipulation.

Yet, an underused part of these datasets are the rich, natural language annotations accompanying each video. (2/12)

The Voltron framework offers a simple way to use language supervision to shape representation learning, building off of prior work in representations for robotics like MVP (https://t.co/Pb0mk9hb4i) and R3M (https://t.co/o2Fkc3fP0e).

The secret is *balance* (3/12)

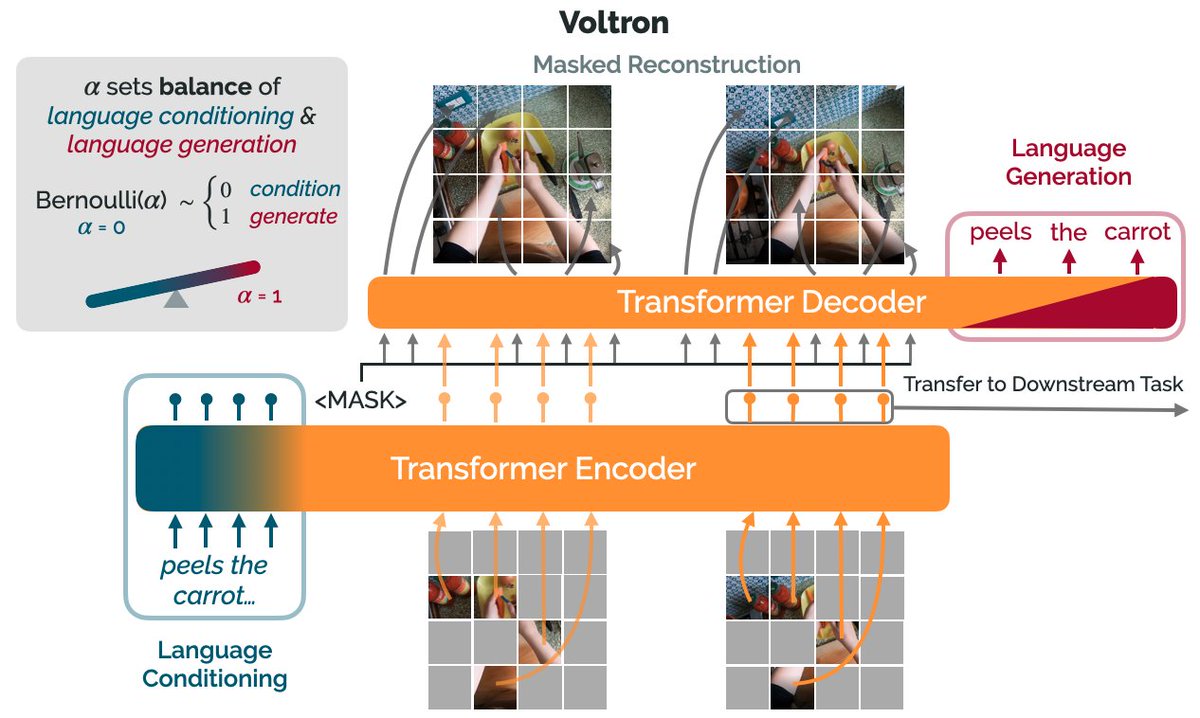

Starting with a masked autoencoder over frames from these video clips, make a choice:

1) Condition on language and improve our ability to reconstruct the scene.

2) Generate language given the visual representation and improve our ability to describe what's happening. (4/12)

By trading off *conditioning* and *generation* we show that we can learn 1) better representations than prior methods, and 2) explicitly shape the balance of low and high-level features captured.

Why is the ability to shape this balance important? (5/12)

Introducing Voltron: Language-Driven Representation Learning for Robotics!

Paper: https://t.co/gIsRPtSjKz

Models: https://t.co/NOB3cpATYG

Evaluation: https://t.co/aOzQu95J8z

🧵👇(1 / 12)

Videos of humans performing everyday tasks (Something-Something-v2, Ego4D) offer a rich and diverse resource for learning representations for robotic manipulation.

Yet, an underused part of these datasets are the rich, natural language annotations accompanying each video. (2/12)

The Voltron framework offers a simple way to use language supervision to shape representation learning, building off of prior work in representations for robotics like MVP (https://t.co/Pb0mk9hb4i) and R3M (https://t.co/o2Fkc3fP0e).

The secret is *balance* (3/12)

Starting with a masked autoencoder over frames from these video clips, make a choice:

1) Condition on language and improve our ability to reconstruct the scene.

2) Generate language given the visual representation and improve our ability to describe what's happening. (4/12)

By trading off *conditioning* and *generation* we show that we can learn 1) better representations than prior methods, and 2) explicitly shape the balance of low and high-level features captured.

Why is the ability to shape this balance important? (5/12)

1. Mini Thread on Conflicts of Interest involving the authors of the Nature Toilet Paper:

https://t.co/VUYbsKGncx

Kristian G. Andersen

Andrew Rambaut

Ian Lipkin

Edward C. Holmes

Robert F. Garry

2. Thanks to @newboxer007 for forwarding the link to the research by an Australian in Taiwan (not on

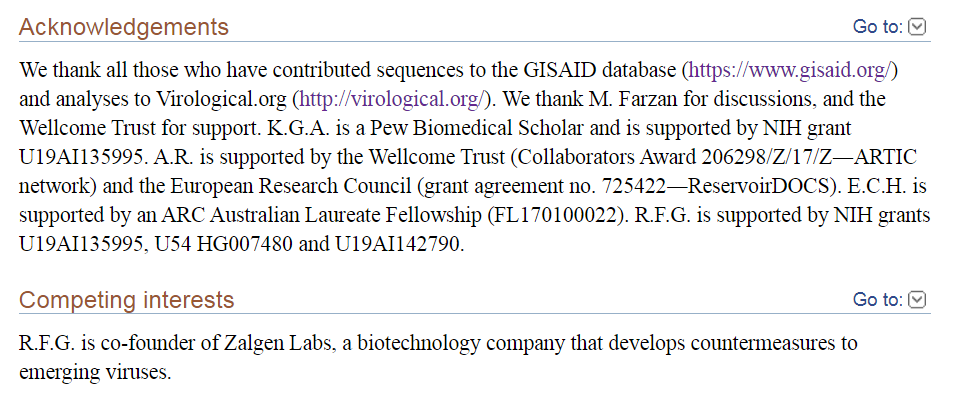

3. K.Andersen didn't mention "competing interests"

Only Garry listed Zalgen Labs, which we will look at later.

In acknowledgements, Michael Farzan, Wellcome Trust, NIH, ERC & ARC are mentioned.

Author affiliations listed as usual.

Note the 328 Citations!

https://t.co/nmOeohM89Q

4. Kristian Andersen (1)

Andersen worked with USAMRIID & Fort Detrick scientists on research, with Robert Garry, Jens Kuhn & Sina Bavari among

5. Kristian Andersen (2)

Works at Scripps Research Institute, which WAS in serious financial trouble, haemorrhaging 20 million $ a year.

But just when the first virus cases were emerging, they received great news.

They issued a press release dated November 27, 2019:

https://t.co/VUYbsKGncx

Kristian G. Andersen

Andrew Rambaut

Ian Lipkin

Edward C. Holmes

Robert F. Garry

2. Thanks to @newboxer007 for forwarding the link to the research by an Australian in Taiwan (not on

3. K.Andersen didn't mention "competing interests"

Only Garry listed Zalgen Labs, which we will look at later.

In acknowledgements, Michael Farzan, Wellcome Trust, NIH, ERC & ARC are mentioned.

Author affiliations listed as usual.

Note the 328 Citations!

https://t.co/nmOeohM89Q

4. Kristian Andersen (1)

Andersen worked with USAMRIID & Fort Detrick scientists on research, with Robert Garry, Jens Kuhn & Sina Bavari among

Our Hans Kristian Andersen working with Jens H. Kuhn, Sina Bavari, Robert F. Garry, Stuart T. Nichol,Gustavo Palacios, Sheli R. Radoshitzky from USAMRIID and Fort Detrick to tell more fairy tales? Full emails listed for queries...https://t.co/kLRoQTxiGD pic.twitter.com/uHNuGraPP2

— Billy Bostickson \U0001f3f4\U0001f441&\U0001f441 \U0001f193 (@BillyBostickson) August 26, 2020

5. Kristian Andersen (2)

Works at Scripps Research Institute, which WAS in serious financial trouble, haemorrhaging 20 million $ a year.

But just when the first virus cases were emerging, they received great news.

They issued a press release dated November 27, 2019: