I recently bought health insurance for few family members. The kind of person I'm, this meant an uncontrollable spiral into research

I read through at-least

- 15 policy documents,

- handbooks+circulars published by IRDAI (the regulatory authority),

- and several blogs

**10 things to remember while buying health insurance**

Now the fun part

The room rent across major Insurers is generally capped to 1% of Sum Insured(SI) per day; which means if your SI is 5 lakh, the insurer WON'T pay more than 5k/day

ICU room charges are generally capped to 2% of SI; which means if your SI is 5 lakh, the insurer will NOT pay more than 10k/day

If you have had experience with ICU charges, 10k/day is nothing for ICU

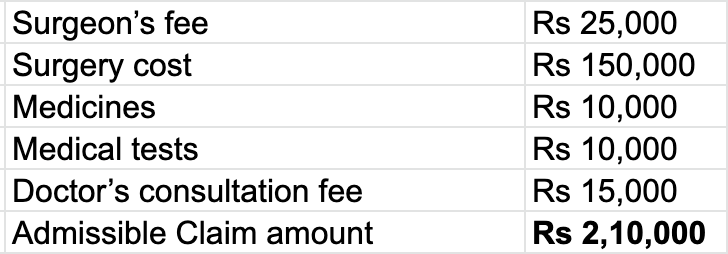

Say you have a SI of 5 lakh, and you had opted for a room within admissible range (5k/day)

Imagine on the day of discharge, you are presented with the final bill as shown

Each of the line items gets reduced in "proportion" of (5/8) = (admissible/actual room rent)

Tragic and funny

You need to be very careful about Co-pay especially if you are buying Insurance for Senior citizens, or folks with critical illness

What that means is, if your admissible claim amount is say 3 lakh, for a Co-pay of 10%, you will have to put up 30k; if claim amount is 5 lakh, you will have to put up 50k. You get the idea

Unfortunate as it is, when she buys an insurance, she CAN'T claim any costs towards hospitalisations@Diabetes till she has waited for at-least

Also, the waiting period differs across diseases & Insurers

**What I did - I looked for a policy that gave me 2 years as waiting period; most insurers give a standard 4 year waiting period

**Make a list of all the pre-existing diseases(PED)/critical diseases specific to the person being insured and factor in the waiting period for those specific diseases

This means, the day I exit my org, the policy expires. Worst, the reverse countdown that had started on my waiting period gets reset!

Fortunately, there's an easy way to tackle this

**Porting - Moving to a new Insurer

Migration - Moving to a new policy within the same Insurer

So say for a family of 3 (1 kid, husband and wife), the total SI could be 5 lakh, which can be claimed by any of the 3 members

On demise of the primary policyholder, the policy ceases to exist for all other members, and they have to buy a new policy at the existing market rates

Many Insurers reward you a 5% CB for every claim free year though I did see policies going as high as 25%

% of CB is important if you are buying insurance early on and also if you are fit. Why?

Say you have an individual insurance with cover of 5 lakh. If you get hospitalised for a medical emergency, and your total expense was 8 lakh, you will have to pay...

Now say everything remains the same, in addition, you also had a top-up policy with a deductible of 5 lakh.

This time, the remaining 3 lakh (claim amount above deductible) will be covered by your top-up policy

ALWAYS go for policies that have "cashless" mode & ALWAYS check for hospitals around you that are included in the PPN.

You May Also Like

MASTER THREAD on Short Strangles.

Curated the best tweets from the best traders who are exceptional at managing strangles.

• Positional Strangles

• Intraday Strangles

• Position Sizing

• How to do Adjustments

• Plenty of Examples

• When to avoid

• Exit Criteria

How to sell Strangles in weekly expiry as explained by boss himself. @Mitesh_Engr

• When to sell

• How to do Adjustments

• Exit

Beautiful explanation on positional option selling by @Mitesh_Engr

Sir on how to sell low premium strangles yourself without paying anyone. This is a free mini course in

1st Live example of managing a strangle by Mitesh Sir. @Mitesh_Engr

• Sold Strangles 20% cap used

• Added 20% cap more when in profit

• Booked profitable leg and rolled up

• Kept rolling up profitable leg

• Booked loss in calls

• Sold only

2nd example by @Mitesh_Engr Sir on converting a directional trade into strangles. Option Sellers can use this for consistent profit.

• Identified a reversal and sold puts

• Puts decayed a lot

• When achieved 2% profit through puts then sold

Curated the best tweets from the best traders who are exceptional at managing strangles.

• Positional Strangles

• Intraday Strangles

• Position Sizing

• How to do Adjustments

• Plenty of Examples

• When to avoid

• Exit Criteria

How to sell Strangles in weekly expiry as explained by boss himself. @Mitesh_Engr

• When to sell

• How to do Adjustments

• Exit

1. Let's start option selling learning.

— Mitesh Patel (@Mitesh_Engr) February 10, 2019

Strangle selling. ( I am doing mostly in weekly Bank Nifty)

When to sell? When VIX is below 15

Assume spot is at 27500

Sell 27100 PE & 27900 CE

say premium for both 50-50

If bank nifty will move in narrow range u will get profit from both.

Beautiful explanation on positional option selling by @Mitesh_Engr

Sir on how to sell low premium strangles yourself without paying anyone. This is a free mini course in

Few are selling 20-25 Rs positional option selling course.

— Mitesh Patel (@Mitesh_Engr) November 3, 2019

Nothing big deal in that.

For selling weekly option just identify last week low and high.

Now from that low and high keep 1-1.5% distance from strike.

And sell option on both side.

1/n

1st Live example of managing a strangle by Mitesh Sir. @Mitesh_Engr

• Sold Strangles 20% cap used

• Added 20% cap more when in profit

• Booked profitable leg and rolled up

• Kept rolling up profitable leg

• Booked loss in calls

• Sold only

Sold 29200 put and 30500 call

— Mitesh Patel (@Mitesh_Engr) April 12, 2019

Used 20% capital@44 each

2nd example by @Mitesh_Engr Sir on converting a directional trade into strangles. Option Sellers can use this for consistent profit.

• Identified a reversal and sold puts

• Puts decayed a lot

• When achieved 2% profit through puts then sold

Already giving more than 2% return in a week. Now I will prefer to sell 32500 call at 74 to make it strangle in equal ratio.

— Mitesh Patel (@Mitesh_Engr) February 7, 2020

To all. This is free learning for you. How to play option to make consistent return.

Stay tuned and learn it here free of cost. https://t.co/7J7LC86oW0