What I will share are some of the output from a simple model for US 10-year Treasury bond yields.

1/n

I am working on a paper on why interest rates and yields are as low as they are. I will share some preliminary results here.

What I will share are some of the output from a simple model for US 10-year Treasury bond yields.

It is key to me that the model not only is statistically significantly, but is also economically significant. We need to understand economic developments within economic theory.

I have estimated a model for the US 10-year bond yield based on the following fundamental variables.

This of course captures the standard textbook relationship from growth theory (the Solow model) in which there is a positive relationship between real interest rates and real GDP as well as the Fischer equation where nominal interest rates are positive related to inflation.

Population growth (and demographics in general) should be expected to impact yields through numerous channels.

I would particularly highlight the impact on growth, risk appetite and savings. Overall we should expect higher population growth to increase yields.

This reflects the compensation investors would demand for lack of credibility of monetary policy.

This is measure of the slack in the US economy and should overall capture the US business cycle.

Futuremore, I have been playing around with different meausre of debt and leverage in the US economy - both private and public debt. None of these variables however, seem to have a statistically significant impact on US yields and rates.

The reason for this might be that these factors are correlated with growth, inflation and demographics.

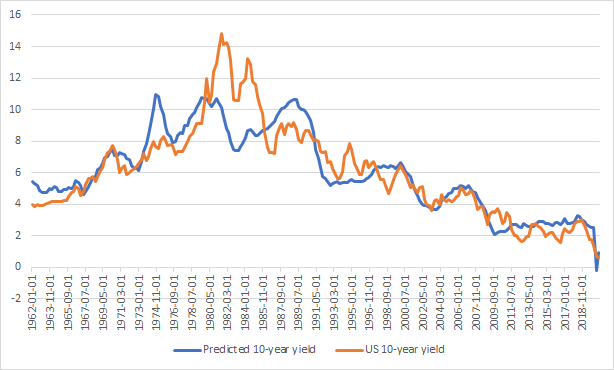

The graph below shows 10-years US yields and the predicted model.

We see the model has quite a good fit over the past nearly 60 years.

We also see that there are some well-known different periods - for example the Great Inflation of the 1970s when yields reached historically high levels and the present period where yields are very low.

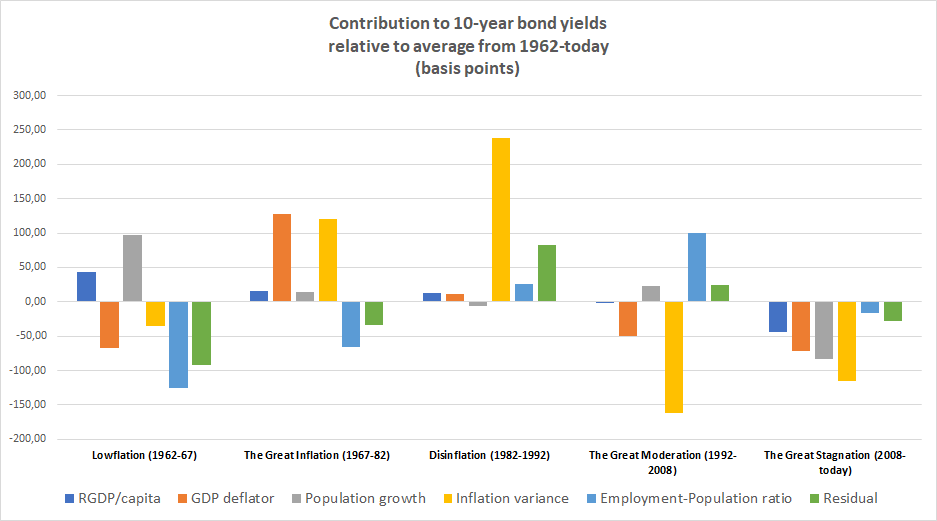

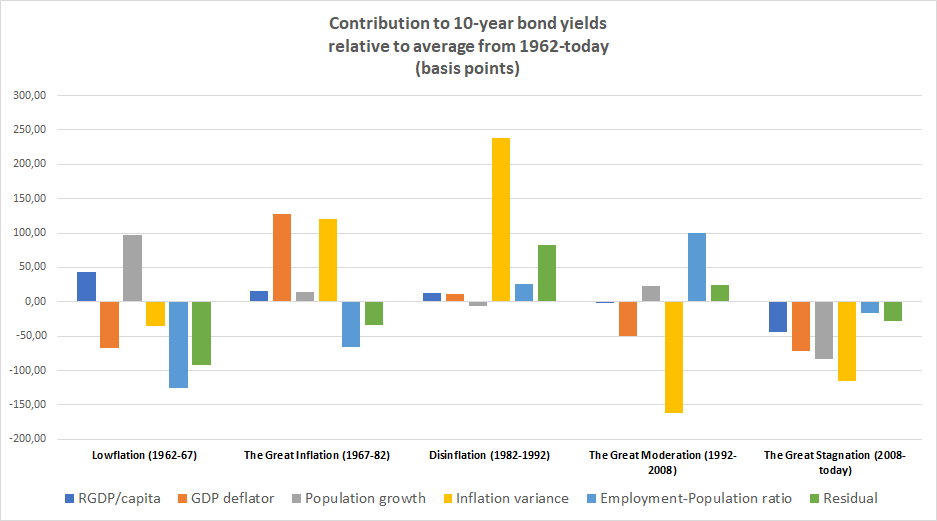

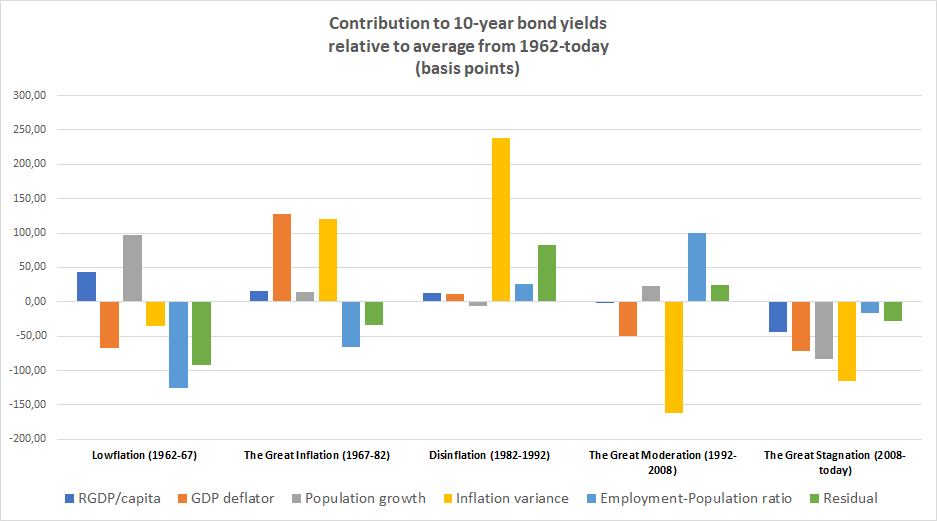

I have looked at the following four periods:

The Great Inflation (1967-82)

Disinflation (1982-1992)

The Great Moderation (1992-2008)

The Great Stagnation (2008-today)

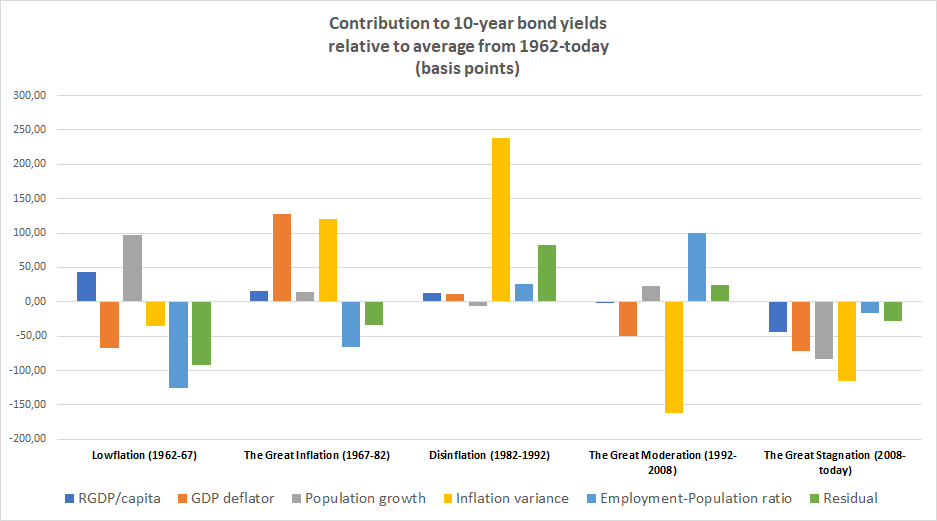

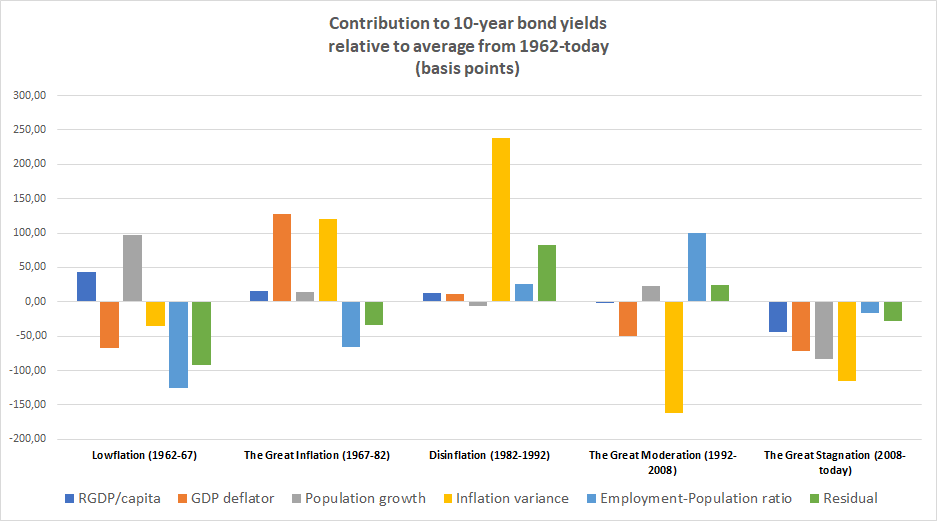

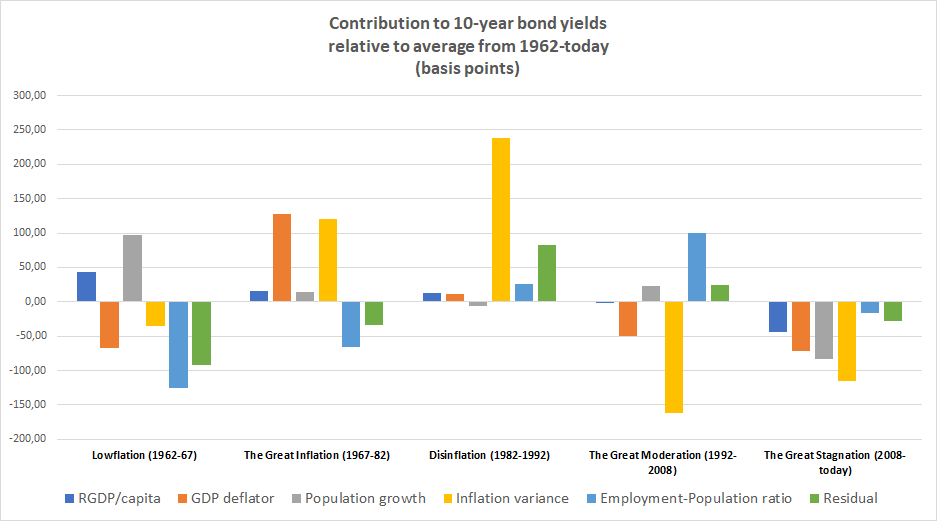

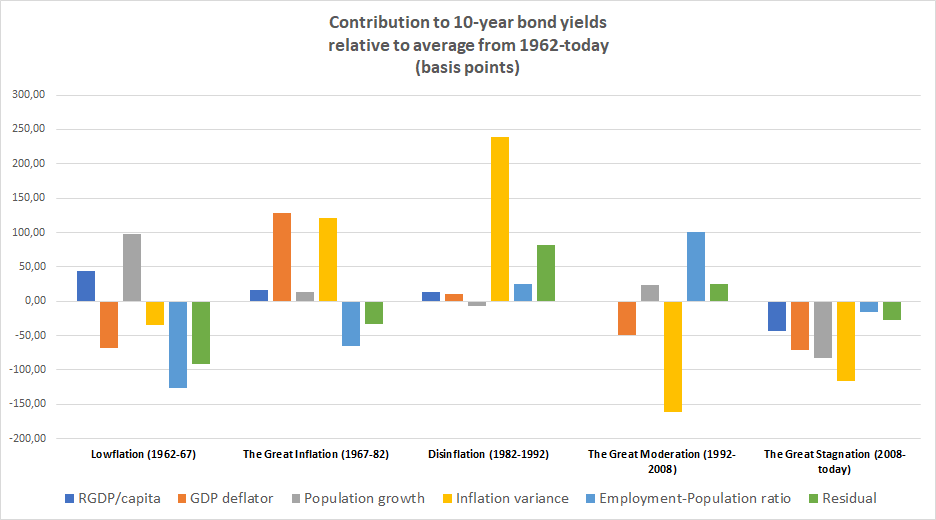

The table below shows the decomposition of the contribution (basis points) to yields from the different factors in the models (note we split NGDP between RGDP growth and inflation).

The decomposition is done RELATIVE to the average impact on yields during the period from 1962 and until today.

Lowflation (1962-67)

During this period yields and rate where low relative to the historical average for the whole estimation period.

We that during the Lowflation period inflation was as was inflation variance. Hence, we had a period of nominal stability as well as some slack in the US economy with higher population growth than employment growth.

...

Higher RGDP/cap growth and pop. growth on the other hand were contributing to higher yields during the lowflation period but the other factors where stronger resulting in overall low yields in this period.

The Great Inflation started around 1967 and ended around 1982.

During this period US-yields and rates rose to historically high levels and the main driver was significant monetary instability with rising and volatile US inflation.

It is notable that during this period not only higher inflation pushed up yields, but equally inflation variance contributed to a similar degree to higher yields. We here see that the lose of monetary policy credibility is very costly.

In 1979 Paul Volcker became Federal Reserve chairman and the following year initiated an effort to reestablish monetary policy credibility and to push down inflation.

However, we here date the disinflation period from 1982 and until 1992.

The Fed's efforts paid off and inflation dropped markedly during this period relative to the Great Inflation period.

However, it is notable that bond yields did not immediately drop to reflect 1-to-1 and inflation variance - measured as 10-year moving variance in quarter/quarter changes in the GDP deflation remained high.

One can of course discuss this measure, but it seems to pretty well capture the fact that it took time to gain credibility about the Fed's renewed commitment to low inflation .

Hence, we see that this lack of credibility measured as inflation variance kept 10-year yields nearly 250bp higher than it would have been if the Fed had had the kind of credibility it had during the 1960s or after 1992.

More from For later read

I should mention, this is why I keep talking about this. Because I know so many people who legally CAN'T.

How do I know they have NDAs, if they can't talk legally about them? Because they trusted me with their secrets... after I said something. That's how they knew I was safe.

Some of the people who have reached out to me privately have been sitting with the pain of what happened to them and the regret that they signed for YEARS. But at the time, it didn't seem like they had any other option BUT to sign.

I do not blame *anyone* for signing an NDA, especially when it's attached to a financial lifeline. When you feel like your family's wellbeing is at stake, you'll do anything -- even sign away your own voice -- to provide for them. That's not a "choice"; that's survival.

And yes, many of the people whose stories I now know were pressured into signing an NDA by my husband's ex-employer. Some of whom I *never* would have guessed. People I thought "left well." Turns out, they've just been *very* good at abiding by the terms of their NDA.

(And others who have reached out had similar experiences with other Christian orgs. Turns out abuse, and the use of NDAs to cover up that abuse, is rampant in a LOT of places.)

How do I know they have NDAs, if they can't talk legally about them? Because they trusted me with their secrets... after I said something. That's how they knew I was safe.

And if the environment at the org was toxic or abusive, it is not uncommon to not realize the extent of that toxicity/abuse until after you're out. But by the time you realize that you signed under duress and presumed good faith where none existed, you're out of options.

— Lauren Thoman (@LaurenThoman) February 16, 2021

Some of the people who have reached out to me privately have been sitting with the pain of what happened to them and the regret that they signed for YEARS. But at the time, it didn't seem like they had any other option BUT to sign.

I do not blame *anyone* for signing an NDA, especially when it's attached to a financial lifeline. When you feel like your family's wellbeing is at stake, you'll do anything -- even sign away your own voice -- to provide for them. That's not a "choice"; that's survival.

And yes, many of the people whose stories I now know were pressured into signing an NDA by my husband's ex-employer. Some of whom I *never* would have guessed. People I thought "left well." Turns out, they've just been *very* good at abiding by the terms of their NDA.

(And others who have reached out had similar experiences with other Christian orgs. Turns out abuse, and the use of NDAs to cover up that abuse, is rampant in a LOT of places.)

Excited we finally have a draft of this paper, which attempts to provide a 'unifying theory' of the long economic divergence between the Middle East & Western Europe

As we see it, there are 3 recent theories that hit on important aspects of the divergence...

1/

One set of theories focus on the legitimating power of Islam (Rubin, @prof_ahmetkuru, Platteau). This gave religious clerics greater power, which pulled political resources away form those encouraging economic development

But these theories leave some questions unanswered...

2/

Religious legitimacy is only effective if people

care what religious authorities dictate. Given the economic consequences, why do people remain religious, and thereby render religious legitimacy effective? Is religiosity a cause or a consequence of institutional arrangements?

3/

Another set of theories focus on the religious proscriptions of Islam, particular those associated with Islamic law (@timurkuran). These laws were appropriate for the setting they formed but had unforeseeable consequences and failed to change as economic circumstances changed

4/

There are unaddressed questions here, too

Muslim rulers must have understood that Islamic law carried proscriptions that hampered economic development. Why, then, did they continue to use Islamic institutions (like courts) that promoted inefficiencies?

5/

As we see it, there are 3 recent theories that hit on important aspects of the divergence...

1/

New CEPR Discussion Paper - DP15802

— CEPR (@cepr_org) February 14, 2021

Culture, Institutions & the Long Divergence@albertobisin @nyuniversity, Jared Rubin @jaredcrubin @ChapmanU, Avner Seror @SerorAvner @amseaixmars @univamu, Thierry Verdier @PSEinfohttps://t.co/lhs6AJb7jE#CEPR_DE, #CEPR_EH, #CEPR_ITRE pic.twitter.com/FtMzAELljJ

One set of theories focus on the legitimating power of Islam (Rubin, @prof_ahmetkuru, Platteau). This gave religious clerics greater power, which pulled political resources away form those encouraging economic development

But these theories leave some questions unanswered...

2/

Religious legitimacy is only effective if people

care what religious authorities dictate. Given the economic consequences, why do people remain religious, and thereby render religious legitimacy effective? Is religiosity a cause or a consequence of institutional arrangements?

3/

Another set of theories focus on the religious proscriptions of Islam, particular those associated with Islamic law (@timurkuran). These laws were appropriate for the setting they formed but had unforeseeable consequences and failed to change as economic circumstances changed

4/

There are unaddressed questions here, too

Muslim rulers must have understood that Islamic law carried proscriptions that hampered economic development. Why, then, did they continue to use Islamic institutions (like courts) that promoted inefficiencies?

5/