The ECB's long-standing negative rates policy remains unpopular in a union of chronic high savings (demand deficits) & yield-hungry investors. Here I argue that the ECB must do everything it can to escape its liquidity trap of “negative rates forever” CC @elerianm @VMRConstancio

There\u2019s a strong case to be made for allowing eurozone borrowing costs to fall lower, says @komileva https://t.co/bO86NHutqs

— Bloomberg Opinion (@bopinion) December 14, 2020

In reality, the Eurozone needs lower real medium-term rates, in order to secure a strong reflationary recovery with market stability. 16/n

More from For later read

Today's Twitter threads (a Twitter thread).

Inside: Planet Money on HP's myriad ripoffs; Strength in numbers; and more!

Archived at: https://t.co/esjoT3u5Gr

#Pluralistic

1/

On Feb 22, I'm delivering a keynote address for the NISO Plus conference, "The day of the comet: what trustbusting means for digital manipulation."

https://t.co/Z84xicXhGg

2/

Planet Money on HP's myriad ripoffs: Ink-stained wretches of the world, unite!

https://t.co/k5ASdVUrC2

3/

Strength in numbers: The crisis in accounting.

https://t.co/DjfAfHWpNN

4/

#15yrsago Bad Samaritan family won’t return found expensive camera https://t.co/Rn9E5R1gtV

#10yrsago What does Libyan revolution mean for https://t.co/Jz28qHVhrV? https://t.co/dN1e4MxU4r

5/

Inside: Planet Money on HP's myriad ripoffs; Strength in numbers; and more!

Archived at: https://t.co/esjoT3u5Gr

#Pluralistic

1/

On Feb 22, I'm delivering a keynote address for the NISO Plus conference, "The day of the comet: what trustbusting means for digital manipulation."

https://t.co/Z84xicXhGg

2/

Planet Money on HP's myriad ripoffs: Ink-stained wretches of the world, unite!

https://t.co/k5ASdVUrC2

3/

Back in November, I published an article for @EFF about @HP's latest printer-ink ripoff: after offering its customers a free-ink-for-life plan, it unilaterally switched them all to a $1/month-for-life plan.https://t.co/bsc73xPSuo

— Cory Doctorow #BLM (@doctorow) February 18, 2021

1/ pic.twitter.com/tagduPupA5

Strength in numbers: The crisis in accounting.

https://t.co/DjfAfHWpNN

4/

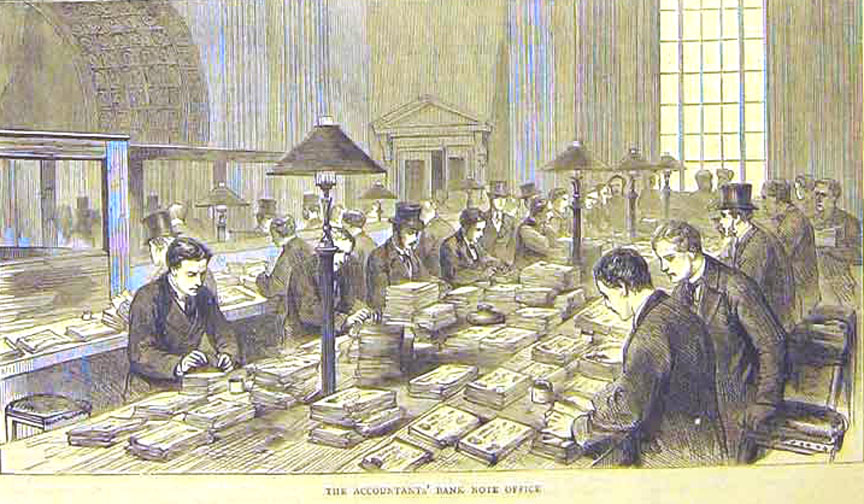

Accountancy is more likely to be mocked than celebrated (or condemned), but accountants, far more than poets, are the unacknowledged legislators of the world.

— Cory Doctorow #BLM (@doctorow) February 18, 2021

1/ pic.twitter.com/FaNQc66gQN

#15yrsago Bad Samaritan family won’t return found expensive camera https://t.co/Rn9E5R1gtV

#10yrsago What does Libyan revolution mean for https://t.co/Jz28qHVhrV? https://t.co/dN1e4MxU4r

5/

I should mention, this is why I keep talking about this. Because I know so many people who legally CAN'T.

How do I know they have NDAs, if they can't talk legally about them? Because they trusted me with their secrets... after I said something. That's how they knew I was safe.

Some of the people who have reached out to me privately have been sitting with the pain of what happened to them and the regret that they signed for YEARS. But at the time, it didn't seem like they had any other option BUT to sign.

I do not blame *anyone* for signing an NDA, especially when it's attached to a financial lifeline. When you feel like your family's wellbeing is at stake, you'll do anything -- even sign away your own voice -- to provide for them. That's not a "choice"; that's survival.

And yes, many of the people whose stories I now know were pressured into signing an NDA by my husband's ex-employer. Some of whom I *never* would have guessed. People I thought "left well." Turns out, they've just been *very* good at abiding by the terms of their NDA.

(And others who have reached out had similar experiences with other Christian orgs. Turns out abuse, and the use of NDAs to cover up that abuse, is rampant in a LOT of places.)

How do I know they have NDAs, if they can't talk legally about them? Because they trusted me with their secrets... after I said something. That's how they knew I was safe.

And if the environment at the org was toxic or abusive, it is not uncommon to not realize the extent of that toxicity/abuse until after you're out. But by the time you realize that you signed under duress and presumed good faith where none existed, you're out of options.

— Lauren Thoman (@LaurenThoman) February 16, 2021

Some of the people who have reached out to me privately have been sitting with the pain of what happened to them and the regret that they signed for YEARS. But at the time, it didn't seem like they had any other option BUT to sign.

I do not blame *anyone* for signing an NDA, especially when it's attached to a financial lifeline. When you feel like your family's wellbeing is at stake, you'll do anything -- even sign away your own voice -- to provide for them. That's not a "choice"; that's survival.

And yes, many of the people whose stories I now know were pressured into signing an NDA by my husband's ex-employer. Some of whom I *never* would have guessed. People I thought "left well." Turns out, they've just been *very* good at abiding by the terms of their NDA.

(And others who have reached out had similar experiences with other Christian orgs. Turns out abuse, and the use of NDAs to cover up that abuse, is rampant in a LOT of places.)

You May Also Like

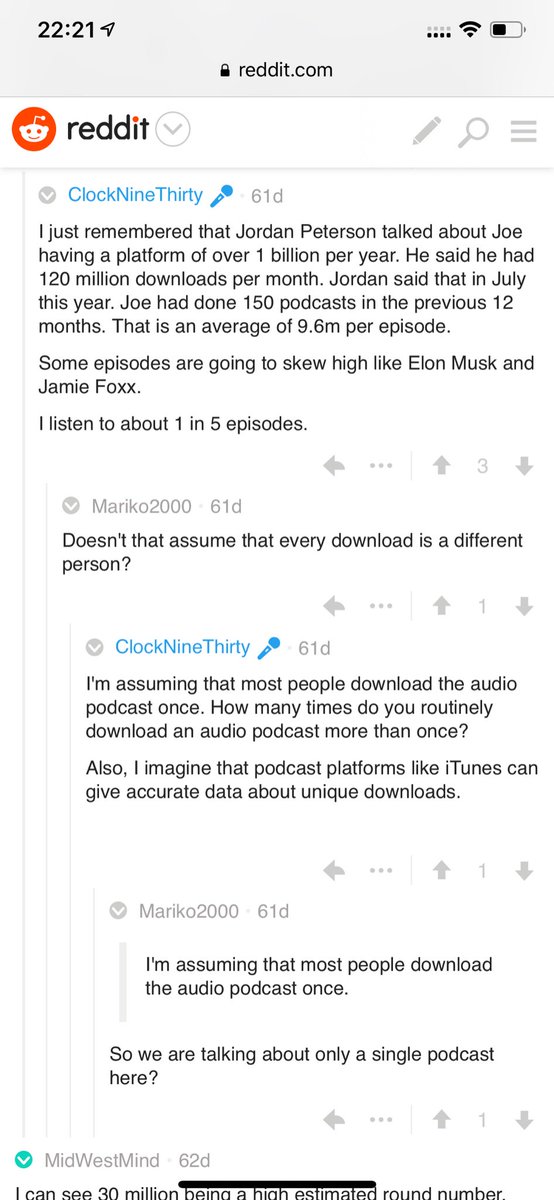

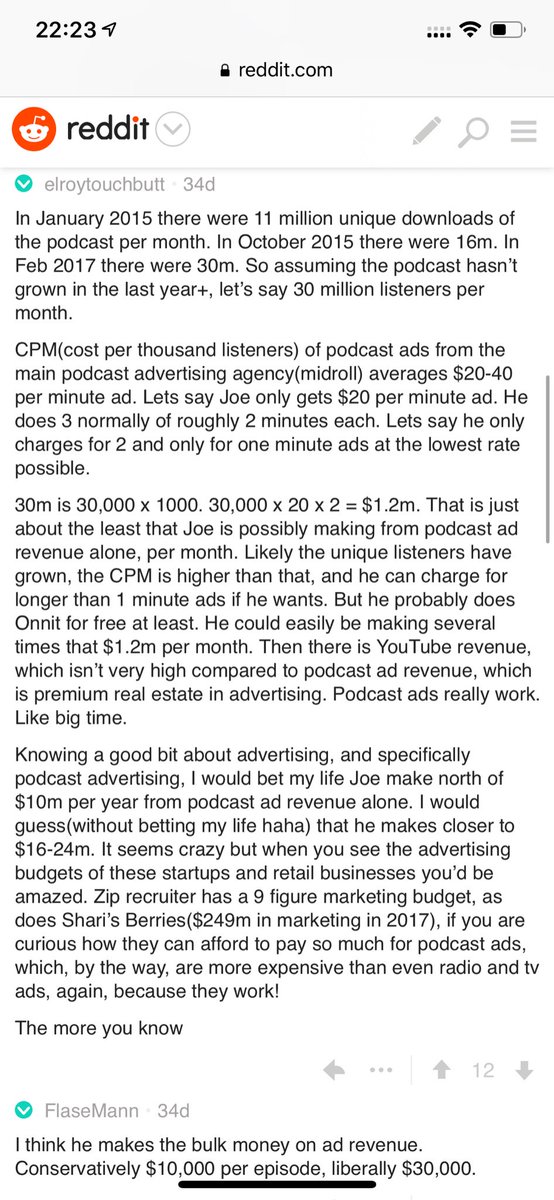

Joe Rogan's podcast is now is listened to 1.5+ billion times per year at around $50-100M/year revenue.

Independent and 100% owned by Joe, no networks, no middle men and a 100M+ people audience.

👏

https://t.co/RywAiBxA3s

Joe is the #1 / #2 podcast (depends per week) of all podcasts

120 million plays per month source https://t.co/k7L1LfDdcM

https://t.co/aGcYnVDpMu

Independent and 100% owned by Joe, no networks, no middle men and a 100M+ people audience.

👏

https://t.co/RywAiBxA3s

Joe is the #1 / #2 podcast (depends per week) of all podcasts

120 million plays per month source https://t.co/k7L1LfDdcM

https://t.co/aGcYnVDpMu