First things first, what does being financially independent mean. When your assets are sufficient to take care of all the future expenses, you are financially independent. This is not synonymous with being rich or wealthy. Also, the first home is not accounted as assets [2/18]

If this sounds vague, park that thought for a while. In my case, my financial assets are 250 times my monthly expenses implying that an annual return of 4% (post-tax) on my investments would cover the monthly expenses while the capital remains intact.

[3/18]

So how did I get there? Being born to parents who are cautious with spending money, averse to debt and financially wise certainly set the foundation right. My dad, who is a medical doctor, explained to me the time value of money when I was 6!

[4/18]

So when I started earning at 21, I was cautious with spending money & saved tiny amounts every month (although didn't invest them wisely). While my savings were limited, I never had to borrow. I did take a car loan when I bought my first car at 28 but closed it in < 1 year [5/18]

But what really propelled my FI journey, which I never chased, were four good decisions I took in my life. The first one being investing in myself. While most of my peers invested in buying homes, I was studying to qualify as an actuary.

[6/18]

Those who know about the profession would appreciate that it is one of the better paying (apart from being amongst the most respected) professions. My salary increased at a rapid pace and expenses at a slower pace. More on delayed gratification later.

[7/18]

The 2nd good decision was to start on my own, which I did in 2017, soon after qualifying as an actuary. The skills gathered while working with corporates for over a decade, decent savings & being 1 amongst 400 actuaries in India was a good enough safety net to quit the job [8/18]

I was lucky to cover more than my opportunity cost in the first year of being on my own. This is where the decision to create my own niche by focussing on helping InsurTechs did the trick. Earned in dollars and saved a lot on taxes.

[9/18]

The fourth and the more recent decision that accelerated the FI journey was shifting my base from Bangalore to Bhilai (a Tier-II/III city), which drastically reduced my expenses. This didn't change my income as most of my InsurTech clients are from overseas.

[10/18]

We have now talked about frugal parents and good decisions. Let's now jump of to delayed gratification, which interestingly has a lot to do with keeping calm!

[11/18]

While I did and continue to pamper myself by staying/dining in 5 stars, vacationing overseas, I got a few things right. I bought Honda Amaze when I could afford Honda City. Invested in ITC when I was craving for an SUV and I am yet to buy a home!

[12/18]

So am I financially independent even though I don't own a home. I am probably not and hence "nearly" in the first tweet. But then I haven't accounted for my crypto assets, investments in start-ups and yes I continue to work!

[13/18]

Financial independence sure seems to in sight though. Thanks to

@dmuthuk, I have now cleaned up my investments & have a lot more efficient portfolio. Tips from

@monikahalan's Let's Talk Money also helped me in being tax-efficient & getting better visibility of my expenses [14/18]

Equally, my downside is substantially covered through the appropriate size of term insurance, health covers (including critical illness, medical, and disability) along with decent emergency funds.

[15/18]

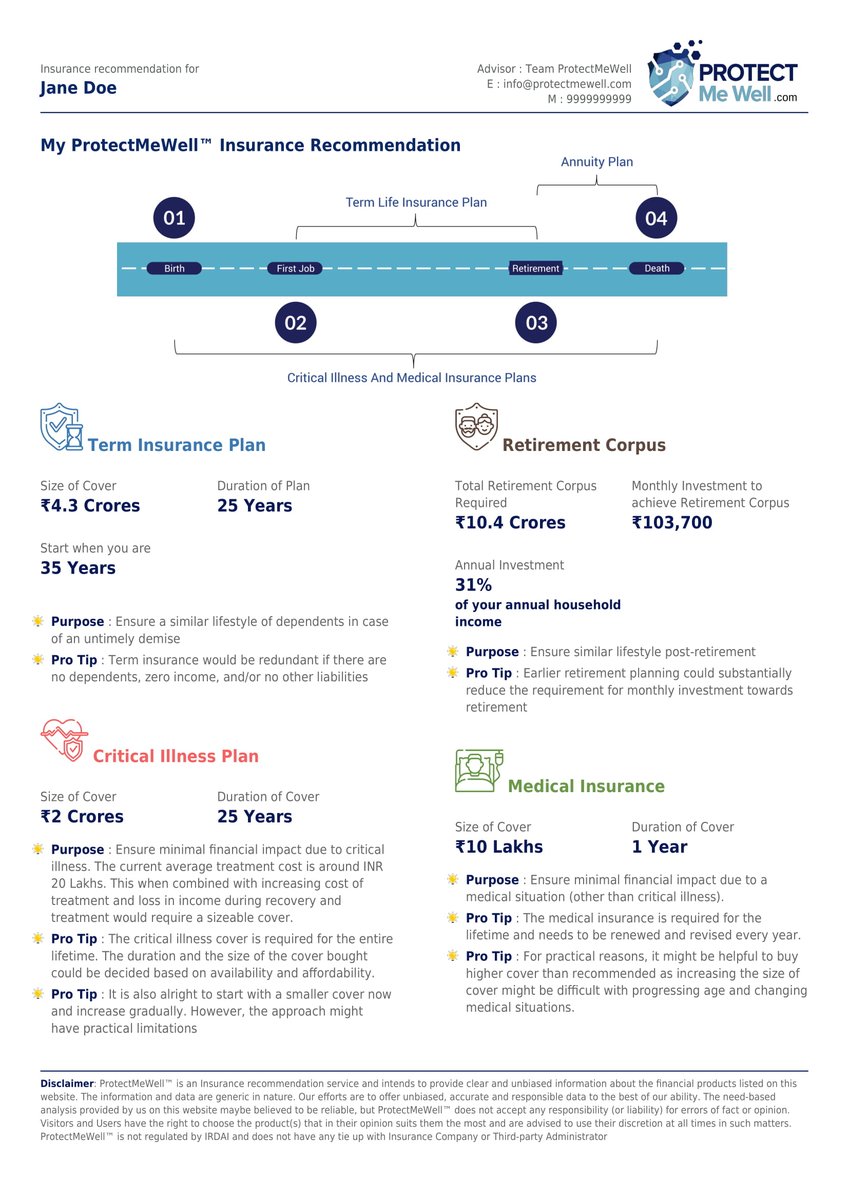

So what does the appropriate size of insurance cover mean? Well, I faced the same question a year ago and had a tough time answering even though I have designed and priced several insurance products in my role of being an actuary.

[16/18]

This is precisely why we did

@ProtectMeWell to help people estimate their insurance needs in an unbiased & scientific manner. We don't sell insurance nor capture any PII (i.e. email id/phone no). However, charge an affordable ₹49 for a personalized report like this

[17/18]

However, for readers of this thread, here is a free link (with limited validity) that bypasses the payment gateway and lets the user take the 1-min journey anonymously.

https://t.co/AdoDOSYbOn Take the journey and set the foundation right for your financial independence.[18/18]

Dear

@dmuthuk &

@monikahalan, @LifeAfterFI this is a thread on my journey of financial independence. Both of you have played crucial parts in it. If you find it useful, please do spread the word and help inspire many more

Here is the link to the first tweet of the thread for your ready reference

https://t.co/mivVRnQU8E