Honestly our prices aren't even high considering the huge amount of work that goes into what we do. What we deserve is to actually be well paid and then get some reparations on top of that lmao

Indigenous beadwork prices are high bc it's reparations

— mango \u2606 (@pamiuqtuq) January 4, 2021

if you can't afford Indigenous made earrings i spend actual time making by hand, maybe go buy cheap earrings from the dollar store or smth because... pic.twitter.com/iHfRhtBX91

— mango \u2606 (@pamiuqtuq) January 4, 2021

More from Finance

1/18 After 3 months, @saffronfinance_ is no longer new on the scene. Now that the kid has climbed the ranks, it's time to see if he can hang with the big boys.

Below are some updated thoughts on potential integrations, improvements, and innovations for Saffron moving forward. ⬇️

2/18 First, if you haven't seen @Privatechad_'s alpha-leaking introductory thread, you should check it out.

I agree that @AlphaFinanceLab and @CreamdotFinance, specifically the Iron Bank, would be ideal targets for SFI risk tranches.

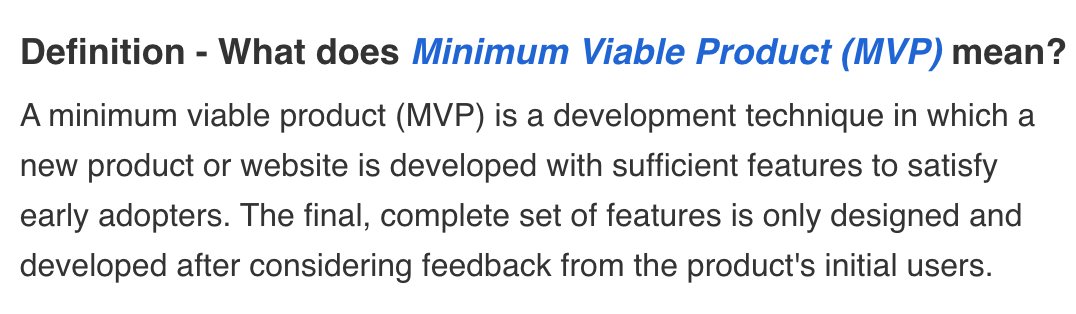

3/18 Speaking more broadly, Saffron is primarily integrated with @compoundfinance, which has served as a MVP of sorts.

The thing is, Compound is one of the safest (but also lowest yield) protocols in DeFi, so it's not surprising that there isn't much demand for the sen. tranche.

4/18 Expanding beyond Compound to higher-risk/higher-return protocols has always been key.

These protocols are the bread-and-butter target market for Saffron, and I would expect to see a surge in demand for senior tranche staking in these

5/18 Additionally, @DeFiGod1 convinced me that Senior Tranche pools would be more appealing if they offered fixed yield.

Essentially, Saffron would augment the product offerings of @Barn_Bridge by also offering senior stakers insurance in the form of junior tranche collateral.

Below are some updated thoughts on potential integrations, improvements, and innovations for Saffron moving forward. ⬇️

1/11 @saffronfinance_ ($SFI) is DeFi's new kid on the block with its tranched yield product that is already live with DAI on @compoundfinance. https://t.co/JpqnxhwrDw

— Benjamin Simon (@benjaminsimon97) November 19, 2020

2/18 First, if you haven't seen @Privatechad_'s alpha-leaking introductory thread, you should check it out.

I agree that @AlphaFinanceLab and @CreamdotFinance, specifically the Iron Bank, would be ideal targets for SFI risk tranches.

15/. 3. Though not the focus atm, interest from various projects and integrations are happening.

— Private Chad (@Privatechad_) February 1, 2021

* Chainlink reached out (props to the amazing $LINK team).

* Talks with $ALPHA and rumored upon V2 releases there will be a collaboration.

*Cream integrations in v2

* $COMP tranches pic.twitter.com/IXCtzvSkw7

3/18 Speaking more broadly, Saffron is primarily integrated with @compoundfinance, which has served as a MVP of sorts.

The thing is, Compound is one of the safest (but also lowest yield) protocols in DeFi, so it's not surprising that there isn't much demand for the sen. tranche.

4/18 Expanding beyond Compound to higher-risk/higher-return protocols has always been key.

These protocols are the bread-and-butter target market for Saffron, and I would expect to see a surge in demand for senior tranche staking in these

4/11 Imo, the golden egg will be vault platforms like @iearnfinance, @picklefinance, etc.

— Benjamin Simon (@benjaminsimon97) November 19, 2020

Recently, some of these higher risk platforms (e.g. @harvest_finance) have been hit with a wave of attacks.

Saffron will enable cautious investors to use these products with peace of mind.

5/18 Additionally, @DeFiGod1 convinced me that Senior Tranche pools would be more appealing if they offered fixed yield.

Essentially, Saffron would augment the product offerings of @Barn_Bridge by also offering senior stakers insurance in the form of junior tranche collateral.

You May Also Like

Trump is gonna let the Mueller investigation end all on it's own. It's obvious. All the hysteria of the past 2 weeks about his supposed impending firing of Mueller was a distraction. He was never going to fire Mueller and he's not going to

Mueller's officially end his investigation all on his own and he's gonna say he found no evidence of Trump campaign/Russian collusion during the 2016 election.

Democrats & DNC Media are going to LITERALLY have nothing coherent to say in response to that.

Mueller's team was 100% partisan.

That's why it's brilliant. NOBODY will be able to claim this team of partisan Democrats didn't go the EXTRA 20 MILES looking for ANY evidence they could find of Trump campaign/Russian collusion during the 2016 election

They looked high.

They looked low.

They looked underneath every rock, behind every tree, into every bush.

And they found...NOTHING.

Those saying Mueller will file obstruction charges against Trump: laughable.

What documents did Trump tell the Mueller team it couldn't have? What witnesses were withheld and never interviewed?

THERE WEREN'T ANY.

Mueller got full 100% cooperation as the record will show.

BREAKING: President Donald Trump has submitted his answers to questions from special counsel Robert Mueller

— Ryan Saavedra (@RealSaavedra) November 20, 2018

Mueller's officially end his investigation all on his own and he's gonna say he found no evidence of Trump campaign/Russian collusion during the 2016 election.

Democrats & DNC Media are going to LITERALLY have nothing coherent to say in response to that.

Mueller's team was 100% partisan.

That's why it's brilliant. NOBODY will be able to claim this team of partisan Democrats didn't go the EXTRA 20 MILES looking for ANY evidence they could find of Trump campaign/Russian collusion during the 2016 election

They looked high.

They looked low.

They looked underneath every rock, behind every tree, into every bush.

And they found...NOTHING.

Those saying Mueller will file obstruction charges against Trump: laughable.

What documents did Trump tell the Mueller team it couldn't have? What witnesses were withheld and never interviewed?

THERE WEREN'T ANY.

Mueller got full 100% cooperation as the record will show.

1/ Some initial thoughts on personal moats:

Like company moats, your personal moat should be a competitive advantage that is not only durable—it should also compound over time.

Characteristics of a personal moat below:

2/ Like a company moat, you want to build career capital while you sleep.

As Andrew Chen noted:

3/ You don’t want to build a competitive advantage that is fleeting or that will get commoditized

Things that might get commoditized over time (some longer than

4/ Before the arrival of recorded music, what used to be scarce was the actual music itself — required an in-person artist.

After recorded music, the music itself became abundant and what became scarce was curation, distribution, and self space.

5/ Similarly, in careers, what used to be (more) scarce were things like ideas, money, and exclusive relationships.

In the internet economy, what has become scarce are things like specific knowledge, rare & valuable skills, and great reputations.

Like company moats, your personal moat should be a competitive advantage that is not only durable—it should also compound over time.

Characteristics of a personal moat below:

I'm increasingly interested in the idea of "personal moats" in the context of careers.

— Erik Torenberg (@eriktorenberg) November 22, 2018

Moats should be:

- Hard to learn and hard to do (but perhaps easier for you)

- Skills that are rare and valuable

- Legible

- Compounding over time

- Unique to your own talents & interests https://t.co/bB3k1YcH5b

2/ Like a company moat, you want to build career capital while you sleep.

As Andrew Chen noted:

People talk about \u201cpassive income\u201d a lot but not about \u201cpassive social capital\u201d or \u201cpassive networking\u201d or \u201cpassive knowledge gaining\u201d but that\u2019s what you can architect if you have a thing and it grows over time without intensive constant effort to sustain it

— Andrew Chen (@andrewchen) November 22, 2018

3/ You don’t want to build a competitive advantage that is fleeting or that will get commoditized

Things that might get commoditized over time (some longer than

Things that look like moats but likely aren\u2019t or may fade:

— Erik Torenberg (@eriktorenberg) November 22, 2018

- Proprietary networks

- Being something other than one of the best at any tournament style-game

- Many "awards"

- Twitter followers or general reach without "respect"

- Anything that depends on information asymmetry https://t.co/abjxesVIh9

4/ Before the arrival of recorded music, what used to be scarce was the actual music itself — required an in-person artist.

After recorded music, the music itself became abundant and what became scarce was curation, distribution, and self space.

5/ Similarly, in careers, what used to be (more) scarce were things like ideas, money, and exclusive relationships.

In the internet economy, what has become scarce are things like specific knowledge, rare & valuable skills, and great reputations.