Thread: Central Pivot Range (CPR)

CPR is another popular tool. Three lines are plotted on the chart when we plot CPR.

The three lines are: CPR, TC and BC.

Let’s understand the calculation.

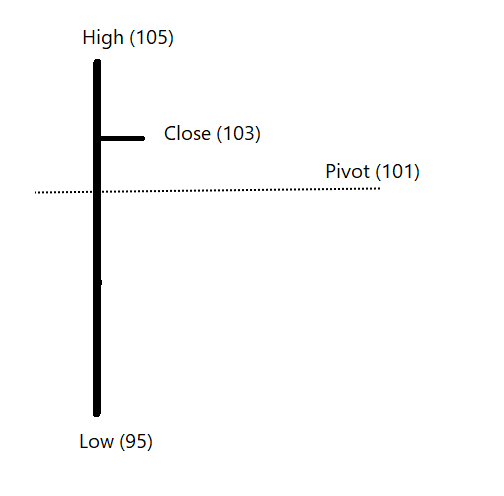

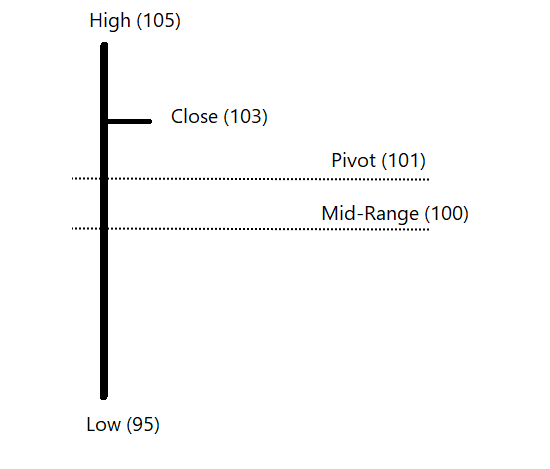

You may recall that I explained the calculation of Pivot levels in an earlier thread. CPR stands for Central Pivot Range. It is always a center line of the three lines that gets plotted in the chart.

CPR is a Pivot price. Pivot is average of HLC as explained in the prev thread.

We also discussed about Mid-range of the session. Mid-range is average of High and low price of the session.

The mid-range of the bar is known as BC in the CPR calculation. BC stands for Bottom central pivot.

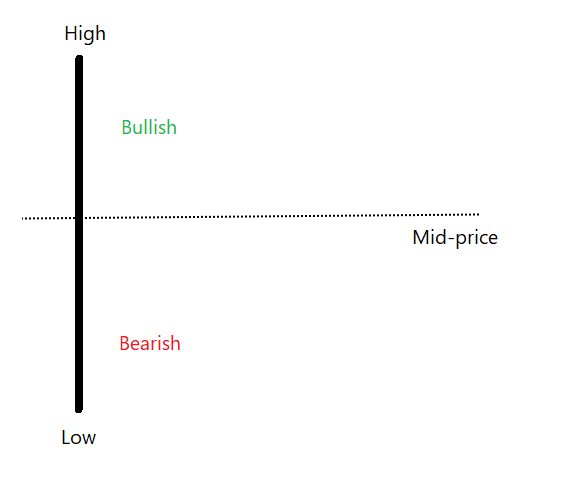

Pivot level captures the relationship of the closing price to the range of the session.

Pivot price above mid-price = bullish pivot

Pivot price below mid-price = bearish pivot

So, CPR line is Pivot and BC line is Mid-range.

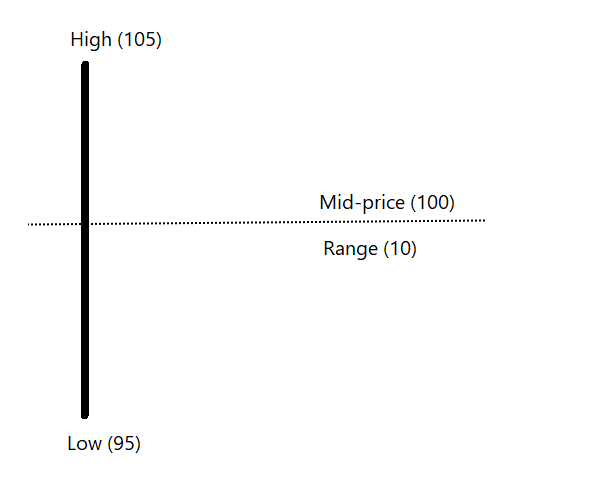

What is the difference between both?

Mid-range is average of High and Low.

Pivot is average of High, Low and Close.

What will make the difference between the two?

Close.