Ahh fuckit part of my @threadapalooza thread had a clear subtopic and wanted to be its own thread.

Here's the thread about "membranes" as a metaphor for groups of people.

15/ One metaphor I've heard people use for regulating group dynamics is of a cell membrane

— Malcolm is back by the \U0001f30ecean! (@Malcolm_Ocean) December 21, 2020

(what's my prompt again? "Spatial metaphors for human systems" ...idk what counts as spatial - everything's pretty spatial to me. I guess I'll avoid computer stuff tho\u2014doing great so far)

- closed membrane

- closed web

- semipermeable membrane

- open network

https://t.co/doandfMsJF

beginning to feel that 'strangely earnest' Twitter is best Twitter

— huan seoul oh (@HuanWin) July 24, 2019

It existed before it had that name.

It overlaps with many other seemingly-unrelated twitter networks.

Rather than joining such a group, you find yourself in it.

https://t.co/z4FO4Nacxu

16/ ...six minutes left, what else is important?

— Malcolm is back by the \U0001f30ecean! (@Malcolm_Ocean) December 21, 2020

I better say something about hierarchy. Hierarchy, as the assymetric organization of things into different functional levels, is a vital part of this beautiful fractal universe.

It can breed power abuses, but so can any context.

More from Economy

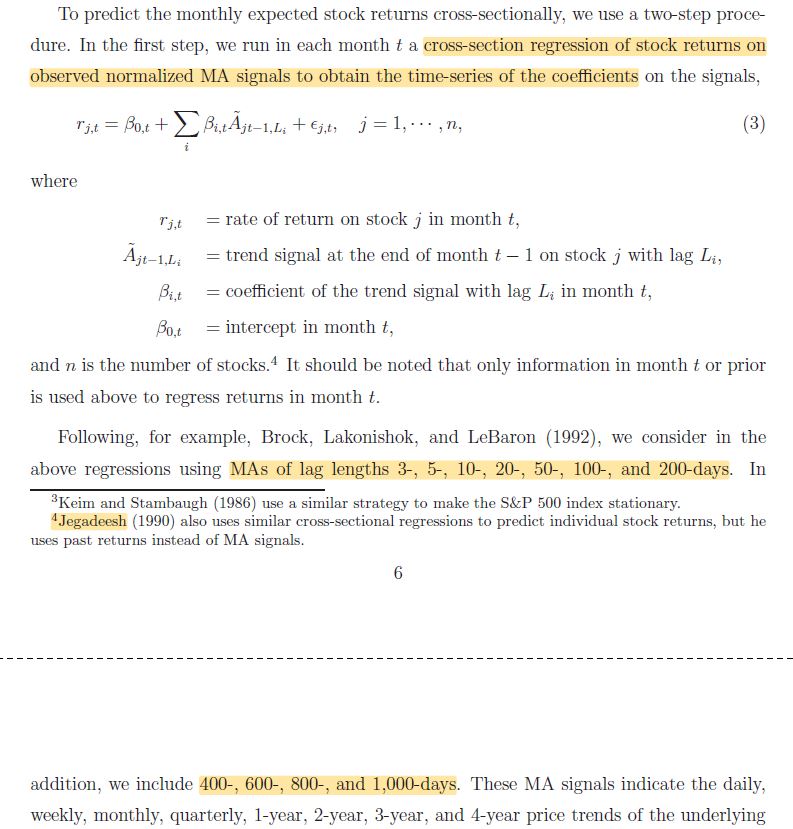

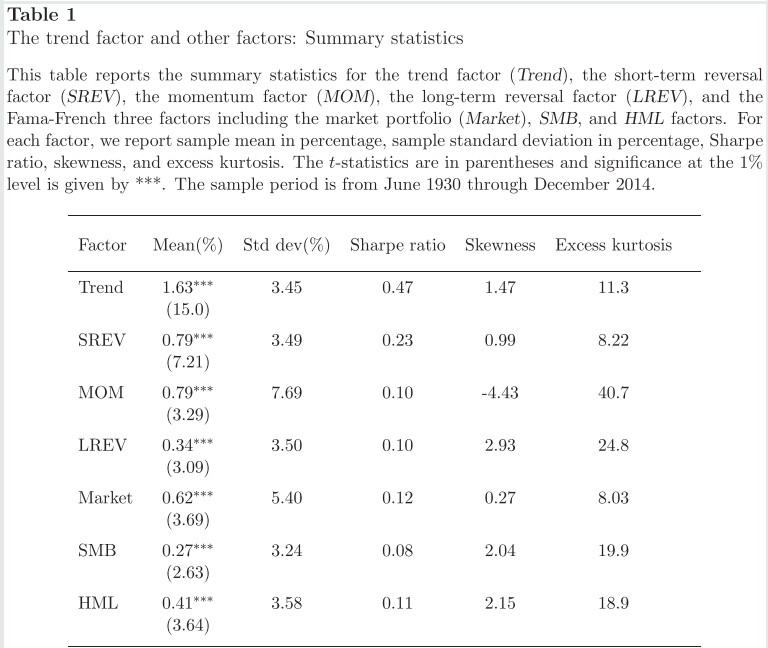

1/ Trend Factor: Any Economic Gains from Using Information over Investment Horizons? (Han, Zhou, Zhu)

"A trend factor using multiple time lengths outperforms ST reversal, momentum, and LT reversal, which are based on the three price trends separately."

https://t.co/udkvsdw2Lz

2/ This resembles combining multiple measures of ST reversal, momentum, and LT reversal (forecasts determined by walking forward rather than using signs from the full sample).

Unlike normal moving average signals, these are *cross-sectional.* More below:

https://t.co/wkIFLg9jtK

3/ Unsurprisingly, the Trend factor formed by this approach outperforms benchmarks in terms of both Sharpe ratio and tail metrics. It's combining momentum with two factors that are negatively correlated to it AND using multiple specifications.

More here:

https://t.co/x8Tloz3iyL

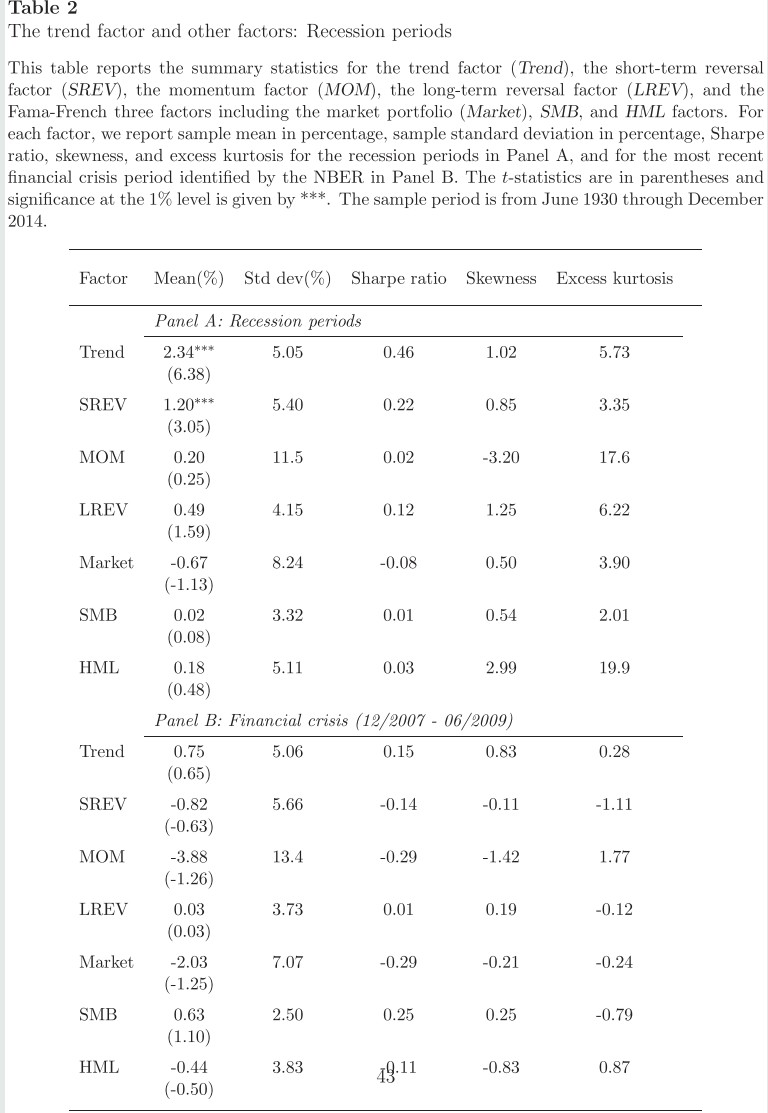

4/ "Average return and volatility of the trend factor are both higher in recession periods. However, the Sharpe ratio is virtually the same.

"Interestingly, all of the factors still have positive average returns.

"Momentum experiences the greatest increase in volatility."

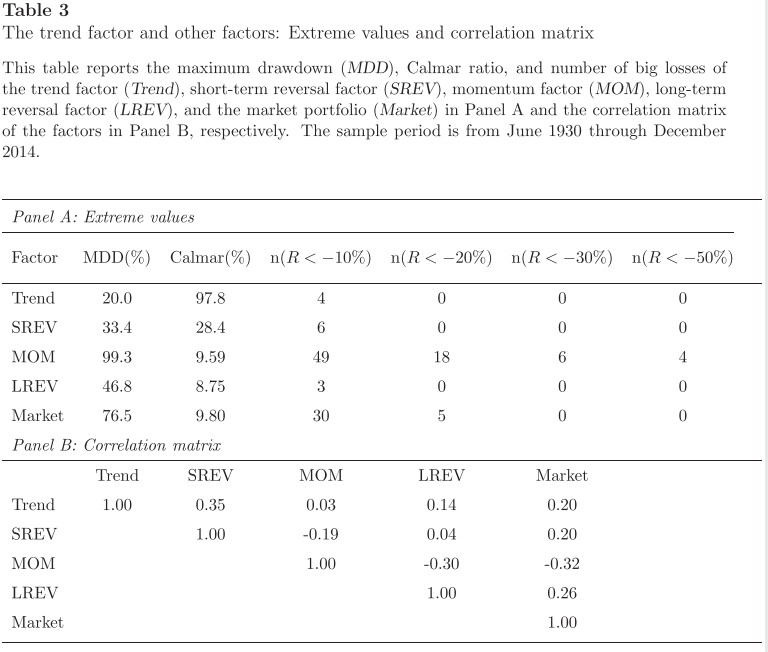

5/ "In terms of maximum drawdown and the Calmar ratio, the trend factor performs the best.

"The trend factor is correlated with the short-term reversal factor (35%), long-term reversal factor (14%), and the market (20%) but is virtually uncorrelated with the momentum factor."

"A trend factor using multiple time lengths outperforms ST reversal, momentum, and LT reversal, which are based on the three price trends separately."

https://t.co/udkvsdw2Lz

2/ This resembles combining multiple measures of ST reversal, momentum, and LT reversal (forecasts determined by walking forward rather than using signs from the full sample).

Unlike normal moving average signals, these are *cross-sectional.* More below:

https://t.co/wkIFLg9jtK

1/ Cross-Sectional and Time-Series Tests of Return Predictability: What Is the Difference? (Goyal, Jegadeesh)

— Darren \U0001f95a (@ReformedTrader) June 18, 2019

"The difference between the performances of TS and CS strategies is largely due to a time-varying net-long investment in risky assets."https://t.co/CSIn3ujN2R pic.twitter.com/XHnVmIart4

3/ Unsurprisingly, the Trend factor formed by this approach outperforms benchmarks in terms of both Sharpe ratio and tail metrics. It's combining momentum with two factors that are negatively correlated to it AND using multiple specifications.

More here:

https://t.co/x8Tloz3iyL

1/ An Executive Summary (in Tweet form) of our new paper

— Adam Butler (@GestaltU) March 27, 2019

Dual Momentum \u2013 A Craftsman\u2019s Perspective

Download here: https://t.co/Y9GlGNohBg

Everything that follows in this thread is based on HYPOTHETICAL AND SIMULATED RESULTS. pic.twitter.com/9m5YJnTdtq

4/ "Average return and volatility of the trend factor are both higher in recession periods. However, the Sharpe ratio is virtually the same.

"Interestingly, all of the factors still have positive average returns.

"Momentum experiences the greatest increase in volatility."

5/ "In terms of maximum drawdown and the Calmar ratio, the trend factor performs the best.

"The trend factor is correlated with the short-term reversal factor (35%), long-term reversal factor (14%), and the market (20%) but is virtually uncorrelated with the momentum factor."